Feb 25, 2023

Feb 25, 2023  Business

Business

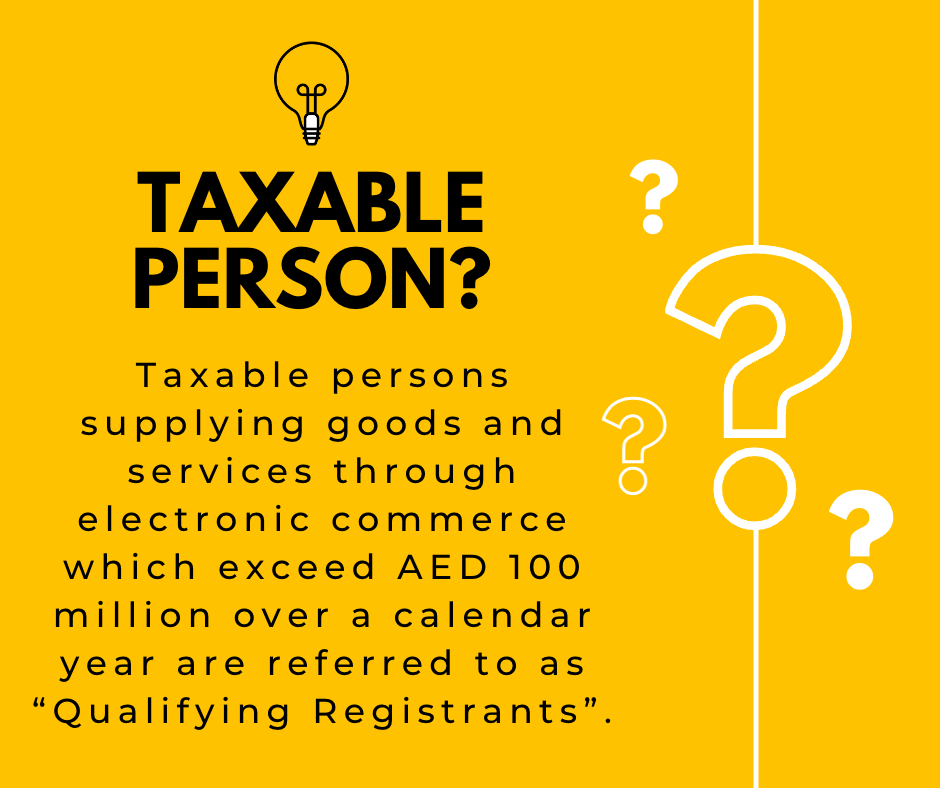

Electronic Commerce Supplies by Qualifying Registrants

From 1 July 2023, Qualifying Registrants are required to report supplies made through e-commerce in box 1 of the VAT Return based on the Emirate in which the supplies of the goods or services are received by the customer, and keep the relevant supporting evidence.

Registrants are required to report taxable supplies subject to VAT at the standard rate, made in each Emirate during a tax period, in the relevant box 1 of the VAT return, covering the tax period in which the supply is made. For Qualifying Registrants, special rules have been introduced to determine the Emirate against which e-commerce supplies are to be recorded and reported for VAT purposes.

For the purposes of Emirates’ reporting, the term “e-commerce” is defined as “the process of selling goods or services through electronic means, an electronic platform, a store in social media, or electronic applications in accordance with criteria and conditions determined by the Minister”.

Electronic means, an electronic platform, a store in social media, or electronic applications are included under the definition of “Electronic Commerce Medium” whereby this definition further covers a website, portal, gateway, interface, platform, marketplace, API and similar applications. Electronic Commerce Medium therefore covers a broad range of concepts, such as stores in the metaverse, smart kiosks, robotic devices, etc.