Feb 28, 2025

Feb 28, 2025  Corporate Tax

Corporate Tax

Tax Deductibility of Payments to Connected Persons: Rules, Conditions, and Documentation

The following important matters are discussed in this article:

- Understanding who qualifies as a connected person to a taxpayer?

- Are payments made to Connected Persons deductible for tax purposes?

- What conditions must be met for these payments to be considered deductible?

- Explore the key supporting documents that a Taxpayer must maintain to substantiate these deductions.

A) Definition of Connected Person to a Taxpayer

- Owner: The person or entity that holds ultimate control and legal rights over the business.

- Shareholders: Individuals or entities that own shares in the company.

- Directors: Appointed to oversee and guide the company’s overall strategy and governance.

- Officers: High-ranking executives responsible for managing the company’s day-to-day operations.

- A partner in an Unincorporated Partnership

- Related parties of people covered above – Includes family members or entities controlled by owners, shareholders, directors, or officers.

B) Deductibility of Payments to connected person

If a person is considered as Connected Person of a Taxable Person, any payments or benefits provided to them are deductible for Corporate Tax purposes only if:

- They reflect the market value of the service or benefit received.

- They are incurred solely and exclusively for the Taxable Person’s business activities.

For instance, if a company grants a rental allowance or housing benefit to its director, officer, or owner, the expense is tax-deductible only if it is in line with the Market Value of comparable accommodations in the same area. Any excess amount paid beyond the market rate may not be considered a deductible expense when calculating Taxable Income. To ensure compliance and fairness, the arm’s length principle must be applied.

The following conditions are considered to demonstrate that payments are made solely for the purpose of business and are in market value.

a) Need for Service:

The service provided by a Connected Person must be essential and directly related to the Taxpayer’s business operations. It should contribute to the company’s core activities, such as management, technical expertise, or strategic guidance. Payments for services that are excessive or unrelated to the business’s needs may not qualify as deductible expenses for tax purposes.

b) Receipt of Service:

The company must have actually received the service for which the remuneration was paid. There should be clear evidence, such as contracts or invoices, that the Connected Person provided a tangible service that benefited the business. Without proof of receipt or a clear link between the payment and the service rendered, the payment may not qualify as a deductible expense.

c) Benefit from Receipt of Service:

The business must demonstrate a clear, measurable benefit from the service provided. This could include improvements in efficiency, cost savings, or enhanced performance directly linked to the service. Without evidence of a tangible benefit to the business, the payment may not qualify as a deductible expense for tax purposes.

d) Expenditure Incurred Wholly and Exclusively for Business Purposes:

The remuneration paid to a Connected Person must be entirely for business-related purposes and should not serve any personal or non-business-related interests. Payments that are partially or wholly for personal benefits, such as personal travel or unrelated services, do not meet the criteria for tax deductibility.

e) Payment Corresponds with Market Value:

The payment made to a Connected Person must reflect fair market rates for similar services, in line with the arm’s length principle. It should be consistent with what would be paid in an open market transaction between unrelated parties. Payments above the market value may be disallowed for tax deduction purposes.

All these conditions must be satisfied for Management Remuneration to qualify as a deductible business expense under corporate tax laws.

C) Arm length Price of payments to connected person:

A transaction or arrangement between Related Parties meets the arm’s length standard if the results of the transaction or arrangement align with what would have been realized if unrelated Persons had engaged in a similar transaction under comparable circumstances.

Market value is determined by considering the amount that would be paid to any third party for similar services under comparable circumstances. For example: Payment to an owner or an independent person for services rendered.

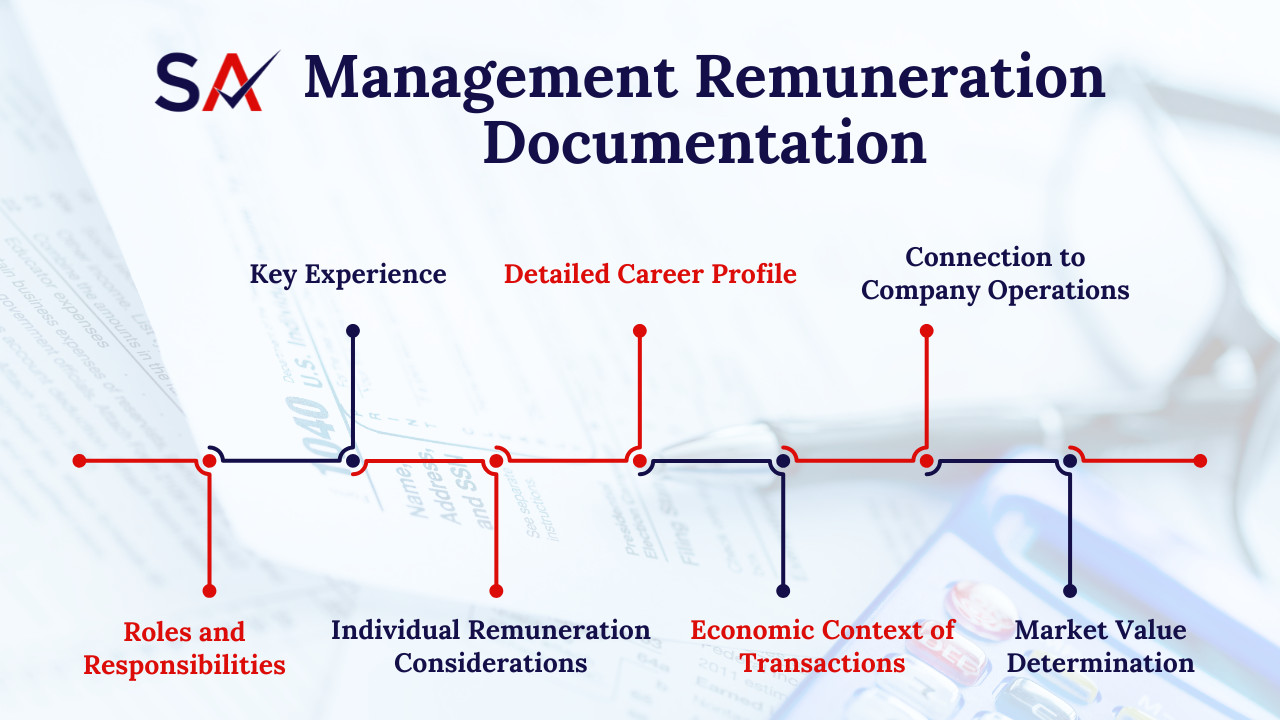

D) Management Remuneration Documentation

To ensure compliance and transparency, proper documentation should be maintained for Owners & Senior Management regarding their Management Remuneration. This includes:

a) Key Experience:

A comprehensive record of their professional background and industry expertise.

b) Detailed Career Profile:

A structured overview of their career journey, highlighting past roles and accomplishments.

c) Connection to Company Operations:

Documentation of their contributions to the business throughout the year and future projections.

d) Roles and Responsibilities:

Clearly defined duties of Directors, CFO, CEO, and other senior executives.

e) Individual Remuneration Considerations:

Relevant in cases where an individual’s skills and expertise are the primary factors in generating profits. Examples include:

- A doctor managing a clinic or polyclinic

- A visiting doctor in a hospital

f) Economic Context of Transactions:

Evaluating the significance of an owner or shareholder actively managing the business versus hiring an external professional, acknowledging the skill set as a key driver of business value.

g) Market Value Determination

Meeting the “functions performed” test to ensure fair market remuneration.

To ensure compliance with corporate tax laws, businesses must adhere to the Arm’s Length Principle while compensating Connected Persons. Proper documentation and adherence to market value standards help avoid tax complications and ensure transparency in financial transactions.

The Taxable Person is responsible for maintaining adequate supporting documentation and ensuring timely submissions to the FTA to substantiate the position taken in the tax return regarding Controlled Transactions within the relevant Tax Period.

Why Choose Spectrum Auditing?

At Spectrum Auditing, we go beyond just being an auditing firm; we’re your trusted partner in navigating the ever-evolving landscape of UAE regulations. Here’s what sets us apart:

- Unparalleled Expertise: Our team consists of accredited auditors, management accountants, consultants with in-depth knowledge of UAE laws, ensuring your business remains compliant.

- Streamlined Solutions: We take a comprehensive approach, guiding you through every step of the process, from risk assessment to filing reports.

- International Recognition: Be audits or any type of compliance, we adhere to the highest standards (ISA, IAS, IFRS), providing global credibility.

- Personalized Support: We understand every business is unique. We tailor our services to address your specific needs and answer any questions you may have.

Partner with Spectrum Auditing today. Let’s focus on your success, while you focus on what you do best – running your business.

Contact us today for a consultation at +971 4 2699329 or email [email protected] to get all our queries addressed.