Sep 03, 2024

Sep 03, 2024  Corporate Tax

Corporate Tax

A Comprehensive Overview of Participation Exemption in UAE Corporate Taxation

To thoroughly understand the concept of participation exemption under UAE corporate tax regulations, it is essential to refer to the following key resources:-

- Ministerial Decision No. 116 of 2023: This decision outlines the participation exemption provisions as specified in the Federal Decree-Law No. 47 of 2022 concerning the taxation of corporations and businesses.

- Article 23 of the Corporate Tax Law: This article details the criteria for exempt and excluded income.

- Guide on Participation Exemption: Provides in-depth guidance on the application of participation exemptions.

Definitions of Participation and Participating Interest:

- Participation:

- Refers to the juridical entity in which the ownership interest is held.

- Participating Interest:

- Denotes an ownership interest in the shares or capital of a juridical person that meets the conditions specified in Article 23 of the Corporate Tax Law.

Conditions for Participation Exemption as per Article 23

Article 23 of the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) addresses the framework for “Exempt Income and Excluded Income.” This article delineates the conditions under which certain types of income are exempt from tax or excluded from taxable income. The primary conditions include:

A Participating Interest typically implies a substantial, long-term stake in a juridical entity, reflecting a degree of control or influence. To qualify as a Participating Interest, the following criteria must be met:

- Minimum Ownership Test: The interest must represent at least 5% ownership in the participating entity.

- Minimum Acquisition Cost Test: Alternatively, the interest must have an acquisition cost of AED 4 million or more.

- Holding Period Test: The interest must be held, or intended to be held, for a continuous period of at least 12 months.

- Subject to Tax Test: The participating entity must be subject to corporate tax or an equivalent foreign tax rate of 9% or higher. Qualifying Free Zone Persons, Exempt Persons, and holding companies may also meet this criterion under specific conditions.

- Entitlement to Profits and Liquidation Proceeds Test: The interest must confer at least 5% of the entity’s profits and liquidation proceeds to the holder.

- Asset Test: No more than 50% of the direct and indirect assets of the participating entity should consist of ownership interests that would not qualify for the participation exemption if held directly.

Let’s understand more clearly with some examples.

Example: 1

Distributions received from a juridical person that is a Resident Person:-

C LLC owns and operates a hotel in the UAE. C LLC’s Accounting Income for the Tax Period was AED 8,000,000. The income was mainly derived from operating the hotels it owns. However, it also owns 50% of F LLC, a UAE resident company. During the Tax Period, F LLC paid C LLC AED 700,000 in dividends. C LLC did not incur any expenditure in relation to its ownership of F LLC. As dividends received from UAE Resident Persons are exempt from Corporate Tax, this amount should be excluded when calculating Taxable Income. C LLC’s Taxable Income (assuming no other adjustments), is therefore AED 7,300,000 (AED 8,000,000 – AED 700,000).

| Item | Details |

| Entity Name | C LLC |

| Business Activity | Hotel Operations in the UAE |

| Accounting Income for the Tax Period | AED 8,000,000 |

| Source of Income | Mainly from hotel operations |

| Ownership in F LLC | 50% |

| Dividend Received From F LLC | AED 700,000 |

| Expenditure Incurred in Relation to F LLC | None |

| Tax Treatment of Dividends | Exempt from Corporate Tax (as F LLC is a UAE Resident) |

| Taxable Income Calculation | AED 8,000,000 – AED 700,000 =AED 7,300,000 |

| Final Taxable Income | AED 7,300,000 |

Example 2:-

Exempt income from a Participating Interest:-

J LLC, a UAE resident company buys a 10% shareholding in K LLC, a juridical person resident in Country A and fully subject to tax in Country A, in the Tax Period ending 31 December 2025 for AED 1,000,000. This 10% shareholding entitles J LLC to receive 10% of K LLC’s distributable profits and 10% of liquidation proceeds (if K LLC is liquidated). In the Tax Period ending 31 December 2026, J LLC receives AED 14,000,000 in cash dividends from K LLC. The dividends will be exempt under the participation exemption. In the Tax Period ending 31 December 2027, J LLC sells part of its shareholding in K LLC, after which it is left with a 3% shareholding in K LLC. The disposal will be exempt under the participation exemption. In the Tax Period ending 31 December 2028, J LLC receives AED 3,000,000 in cash dividends from K LLC. This dividend will not be exempt because the conditions for the Participating Interest are no longer satisfied (i.e. holding 5% or greater, or acquisition cost in excess of AED 4,000,000 in the shareholding and being entitled to receive at least 5% of K LLC’s distributable profits and liquidation proceeds of K LLC).

| Item | Details |

| Entity Name | J LLC |

| Residence | UAE |

| Shareholding in K LLC | 10%(initially) |

| Country of Residence for K LLC | Country A |

| K LLC’s Tax Status in Country A | Fully subject to tax in Country A |

| Acquisition Cost of 10% shareholding | AED 1,000,000 |

| Entitlements from 10% shareholding |

|

| Tax Period Ending 31 December 2026 | |

| Dividends received from K LLC | AED 14,000,000 |

| Tax Treatment of Dividends(2026) | Exempt under the participation exemption |

| Tax Period Ending 31 December 2027 | |

| Disposal of Shareholding in K LLC | Partial sale; J LLC retains 3% shareholding in K LLC |

| Tax Treatment of Disposal | Exempt under the participation exemption |

| Tax Period Ending 31 December 2027 | |

| Dividends received from K LLC | AED 3,000,000 |

| Tax Treatment of Dividends(2028) | Not exempt, as J LLC no longer meets the conditions for the Participating Interest |

| Conditions for Participating Interest |

|

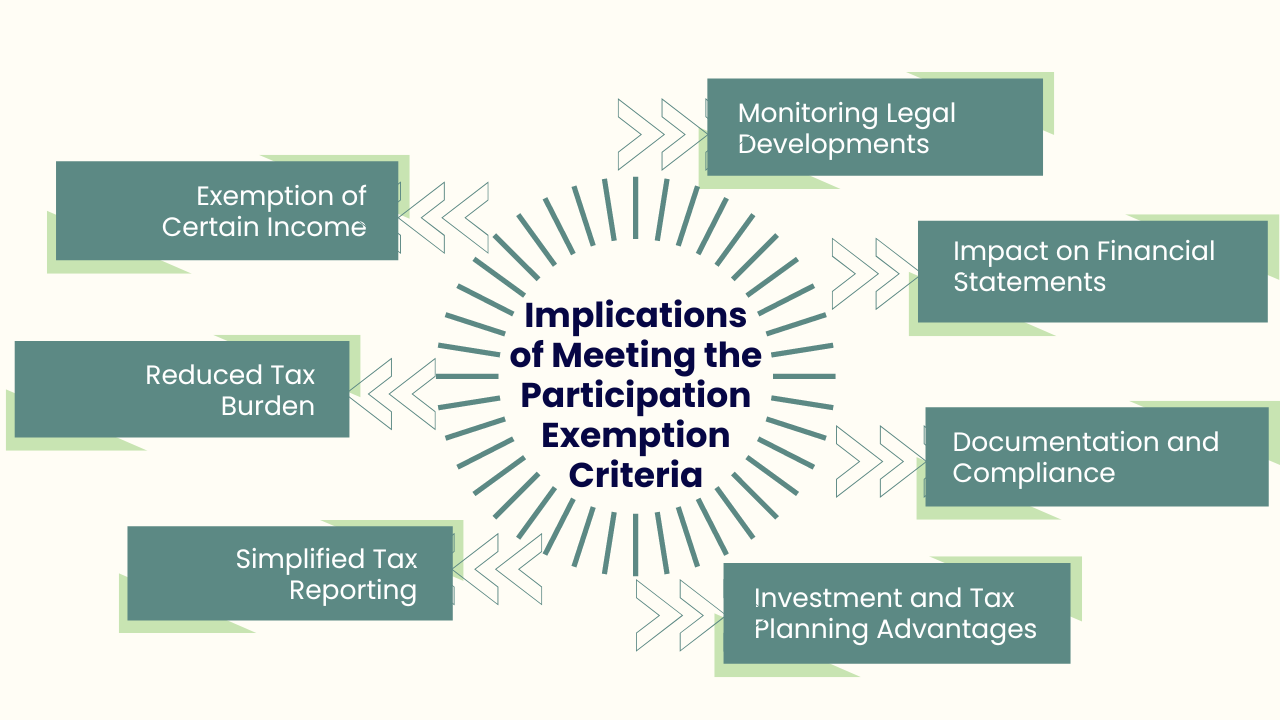

Implications of Meeting the Participation Exemption Criteria

Entities that qualify for the participation exemption under UAE corporate tax laws can benefit in several significant ways:

- Exemption of Certain Income:

Dividends and Profit Distributions: Dividends and profit distributions from qualifying subsidiaries or other entities are exempt from UAE corporate tax if the recipient holds at least 5% of the shares in the subsidiary and the subsidiary is subject to a comparable tax rate in its home jurisdiction.

- Reduced Tax Burden:

Lower Effective Tax Rate: The participation exemption reduces the overall tax burden by excluding certain types of income from taxable profits, resulting in a lower effective tax rate for the entity.

- Simplified Tax Reporting:

Streamlined Compliance: Entities meeting the eligibility criteria may experience simplified reporting requirements for exempt income. However, they must ensure compliance with all regulatory requirements and maintain proper documentation.

- Investment and Tax Planning Advantages:

Strategic Benefits: The exemption facilitates strategic investment and tax planning by mitigating the tax impact of receiving income from investments in subsidiaries or joint ventures.

- Documentation and Compliance:

Record-Keeping: Entities must maintain comprehensive records to substantiate their eligibility for the participation exemption, including evidence of ownership and tax payments made by subsidiaries.

- Impact on Financial Statements:

Financial Reporting: The exemption affects how income is reported in financial statements. Exempt income is excluded from taxable profits, influencing the entity’s financial position and reported tax expense.

- Monitoring Legal Developments:

Regulatory Updates: Entities should stay informed about any changes in tax laws or regulations that could affect the eligibility criteria or conditions for the participation exemption.

Types of Exempt and Excluded Income

Exempt Income:

- Dividends and Profit Distributions: Generally exempt if the recipient holds at least 5% of the shares in a qualifying subsidiary and the subsidiary is subject to a comparable tax rate.

- Income from Certain Government Entities: Income from specific government entities, such as sovereign wealth funds, may be exempt.

- Income from Foreign Sources: Income derived from foreign sources and subject to tax in the relevant jurisdiction may qualify for exemption under certain conditions.

Excluded Income:

- Gains on Disposal of Qualifying Investments: Gains from the sale of qualifying investments might be excluded from taxable income if specific conditions are met.

- Income from Specific Activities: Income from activities covered by particular exemptions, such as charitable or public service operations, may be excluded.

Conditions and Limitations:

- Minimum Ownership Requirements: For dividend exemptions, a minimum ownership threshold, typically 5% of shares, must be satisfied.

- Tax Comparison: The tax rate in the jurisdiction where the income is sourced should be comparable to the UAE corporate tax rate.

- Documentation and Compliance: Proper documentation and adherence to reporting requirements are essential for qualifying for these exemptions and exclusions.

In summary, qualifying for participation exemption under UAE corporate tax laws allows entities to exclude certain types of income from taxable income, thereby reducing their overall tax liability and simplifying tax reporting. However, maintaining eligibility requires adherence to specific conditions and thorough documentation.

Why Choose Spectrum Auditing?

At Spectrum Auditing, we go beyond just being an auditing firm; we’re your trusted partner in navigating the ever-evolving landscape of UAE regulations. Here’s what sets us apart:

- Unparalleled Expertise: Our team consists of accredited auditors, management accountants, consultants with in-depth knowledge of UAE laws, ensuring your business remains compliant.

- Streamlined Solutions: We take a comprehensive approach, guiding you through every step of the process, from risk assessment to filing reports.

- International Recognition: Be audits or any type of compliance, we adhere to the highest standards (ISA, IAS, IFRS), providing global credibility.

- Personalized Support: We understand every business is unique. We tailor our services to address your specific needs and answer any questions you may have.

Partner with Spectrum Auditing today. Let’s focus on your success, while you focus on what you do best – running your business.

Contact us today for a consultation at +971 4 2699329 or email [email protected] to get all our queries addressed.