Jan 17, 2021

Jan 17, 2021  VAT

VAT

Covid-19-Related Rent Concessions Amendment to IFRS 16

IFRS 16, Leases, effective for annual periods beginning on or after 1 January 2019, was amended in response to the COVID-19 coronavirus pandemic by International Accounting Standards Board to provide optional relief to lessees from applying IFRS 16’s guidance on lease modification accounting for rent concessions arising as a direct consequence of the COVID-19 pandemic.

As a result of Covid-19 impact, rent concessions have been provided to the lessees, as the entities across different industries are facing significant challenging circumstances. Such concessions comes in different forms lease concessions which may include rent waivers, payment deferrals, and cash rebates and key assumptions made by lessee on lease period, impairment considerations etc.

The key matter which needs to be focused in the list of various changes is lease concessions, which could arise because of:

- Terms in the lease arrangement or

- Government initiatives or

- Voluntary support extended by Lessor or

- Mutual arrangement between the lessee and the lessor

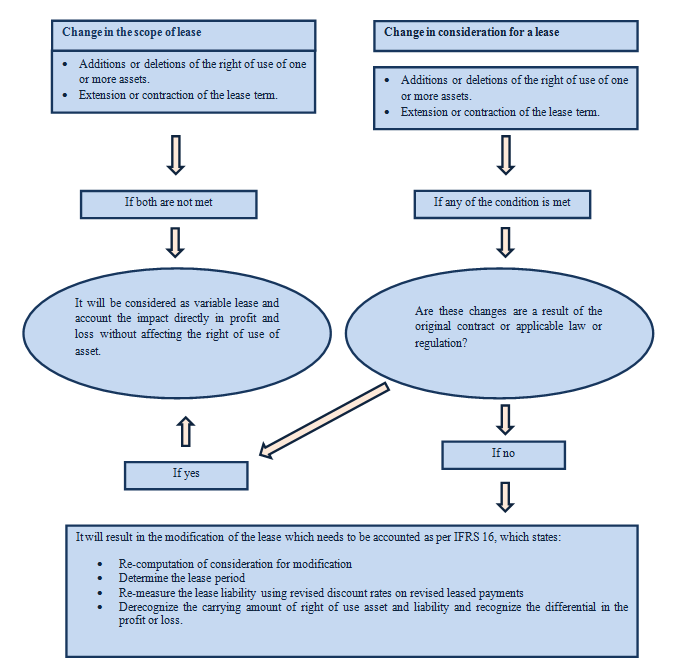

Lease Modification:

A lease modification is defined by IFRS 16 as: A change in the scope of a lease, or The consideration of a lease, that was not a part of the original terms and conditions of the lease.Accounting for lease modification:

There could be several challenges and complications that can arise in each stage.

The following situations will not result in lease modification and will be accounted in the Profit or Loss:

- If the modifications are part of the actual lease arrangement.

- Modifications due to government regulations, resulting into rent concessions which can also fall under force majeure in the agreement.

- Rent Deferrals, without change to overall consideration.

- Entity may need to consider necessary legal interpretation of certain rental arrangement, if needed.