Nov 07, 2024

Nov 07, 2024  Accounting

Accounting

With the implementation of corporate tax in the UAE, companies are now required to adhere to IAS 12 Income Taxes, which governs how income taxes are accounted for in financial statements. This standard ensures that companies accurately reflect current and deferred tax liabilities and assets, impacting their financial reporting transparency and compliance with international accounting standards.

Objective of IAS 12

IAS 12 outlines the accounting treatment for income taxes, addressing both current and future tax consequences of:

- The future recovery or settlement of the carrying amount of assets and liabilities recognized in an entity’s statement of financial position.

- Transactions and other events of the current period recognized in an entity’s financial report.

Current Tax – Recognition and Measurement

IAS 12 requires recognizing current tax in an entity’s financial statements. Unpaid current tax for current and prior periods should be recognized as a liability, while any overpaid amount should be recognized as an asset. These liabilities and assets are determined based on the tax rates enacted or substantively enacted by the end of the reporting period. A corresponding amount is recorded as expense or income in the profit or loss for the period.

i) To recognise the current tax expenses

Journal Entries:

Current tax expense ***

To Provision for Tax (current tax liability) ****

Note: Current tax expense is recognized in profit or loss or other comprehensive income according to the item on which it is created.

Deferred Tax – Recognition and Measurement

Deferred Tax Assets

Deferred tax assets must be recognized for all deductible temporary differences if it is probable that taxable profit will be available to utilize these differences, except when the deferred tax asset arises from the initial recognition of an asset or liability in a transaction that:

- Is not a business combination, and

- At the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

Additionally, deferred tax assets should be recognized for the carry forward of unused tax losses and unused tax credits, but only if it is probable that future taxable profit will be available to utilize these losses and credits.

Deferred Tax Liabilities

A deferred tax liability arises when there is a taxable temporary difference between the tax base of an asset or liability and its carrying amount in the financial statements. This occurs when the carrying amount of an asset exceeds its tax base, meaning the future recovery of the carrying amount will generate taxable profit.

A taxable temporary difference also arises when the carrying amount of a liability is less than its tax base. This is because the future settlement of its tax base will generate taxable profit. For example, this occurs when a loan is initially recognized at fair value net of borrowing costs, but the tax deductions for these costs are amortized over the life of the loan.

Some examples to understand the measurements of deferred tax assets and liabilities

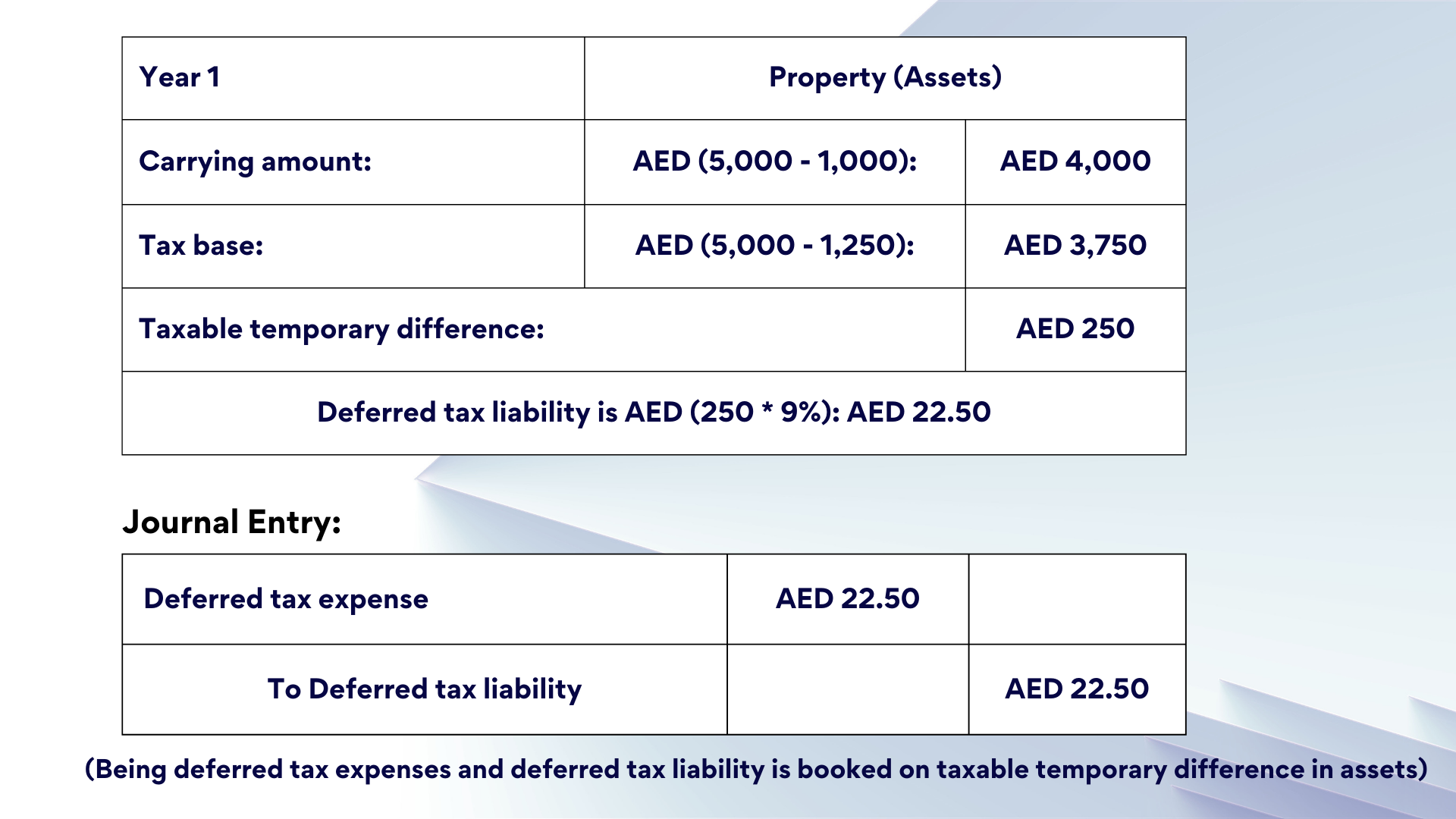

i) A Ltd. purchased a property costing AED 5,000. Depreciation is charged @ 20% p.a. on SLM Basis for accounting purposes. Depreciation is charged @ 25% on SLM basis in corporate tax. Tax rate is 9%.

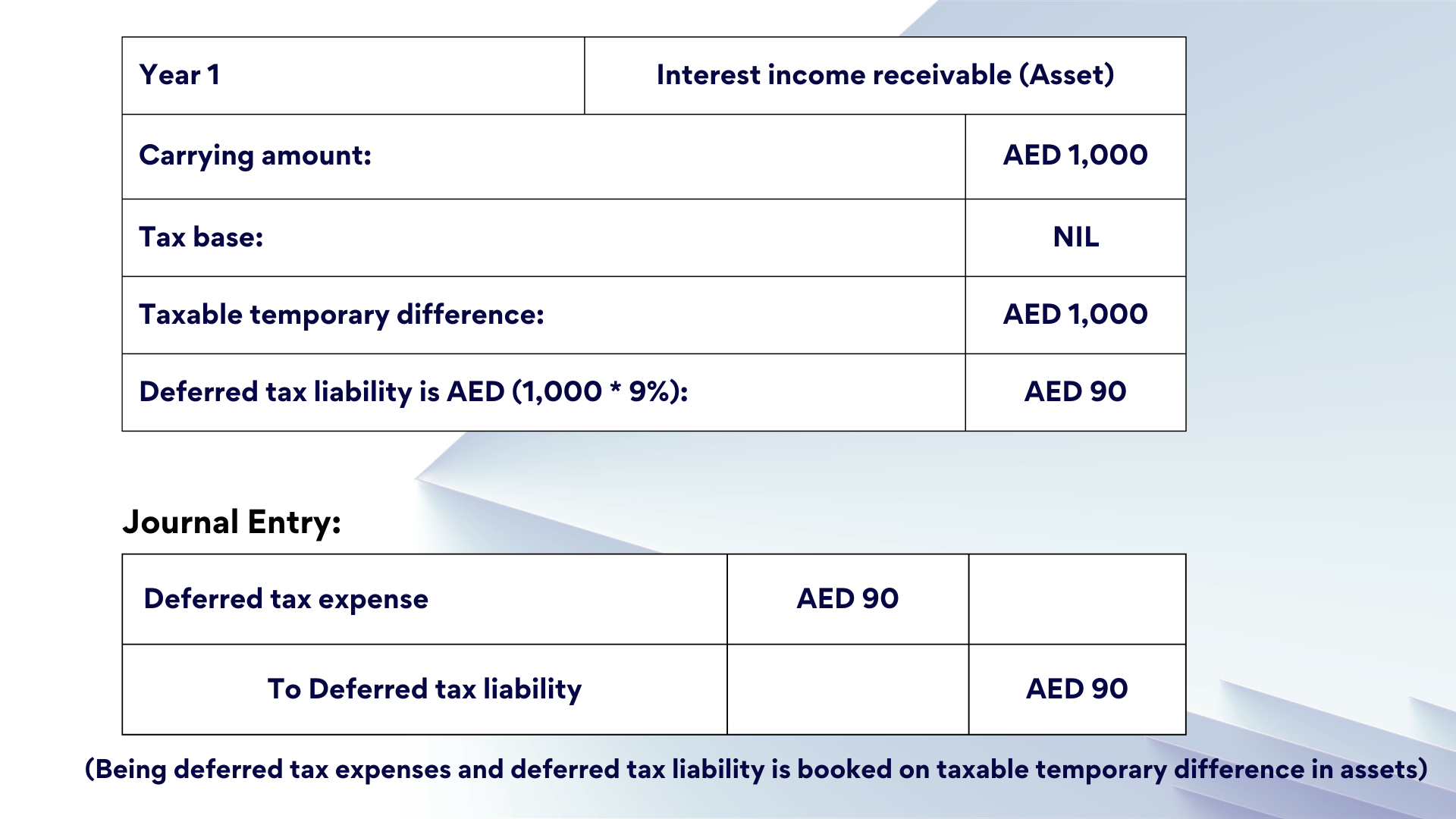

ii) A Ltd has an interest income receivable of AED 1,000. In corporate tax, interest income is taxable on cash basis. Tax rate is 9%.

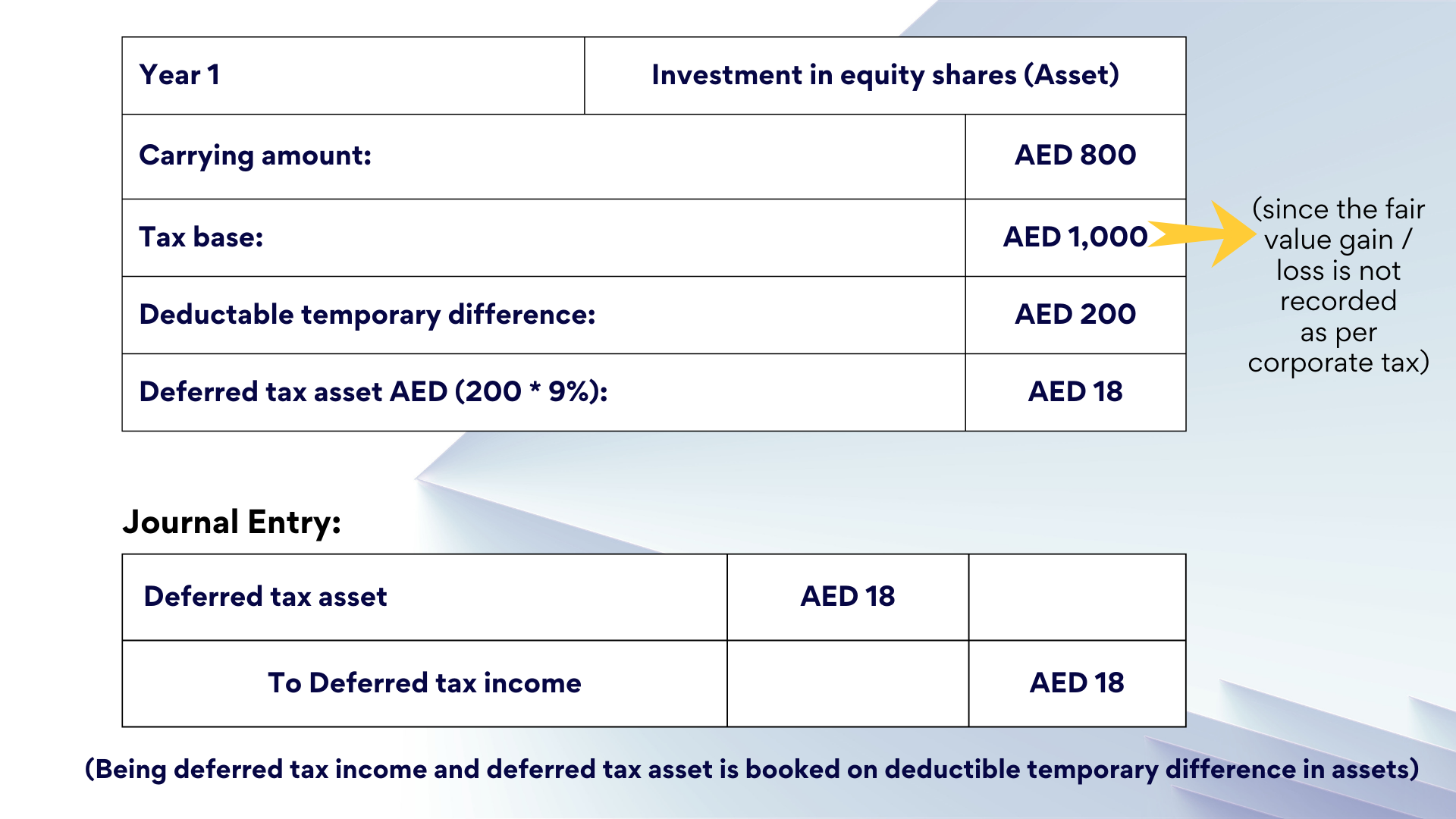

iii) A Ltd. has made an investment in equity shares for AED 1,000. It is shown at FVTPL. At the year’s end, the fair value of investment in equity shares is AED 800. Tax rate is 9%.

iv) A Ltd. has made a provision for a division closure cost of AED 1,000. In corporate tax, closure cost is allowed only when it is paid. The tax rate is 9%.

v) Expenses not deductible/not allowed as per corporate tax (examples: penalties, donations, personal expenses, bribes). No Deferred tax assets/liabilities will be created — it is a permanent difference.

vi) Carried forward losses are deductible temporary differences on which deferred tax assets are created.

Measurement of Deferred Tax Assets and Liabilities

Deferred tax assets and liabilities are measured using the tax rates that have been enacted or substantively enacted and are expected to apply when the asset is realized or the liability is settled.