Jul 01, 2019

Jul 01, 2019  VAT

VAT

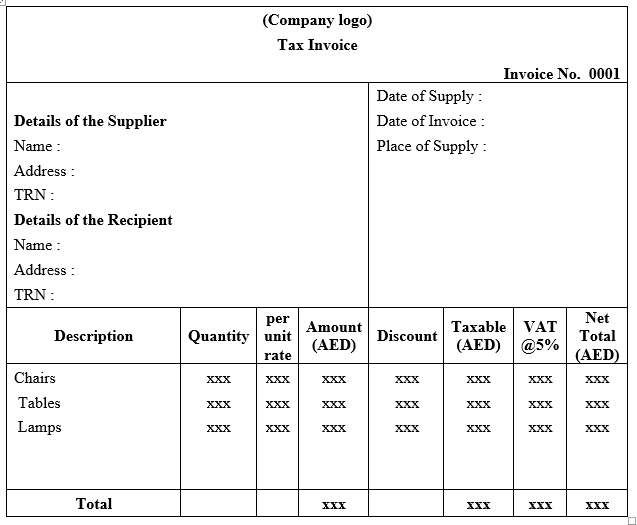

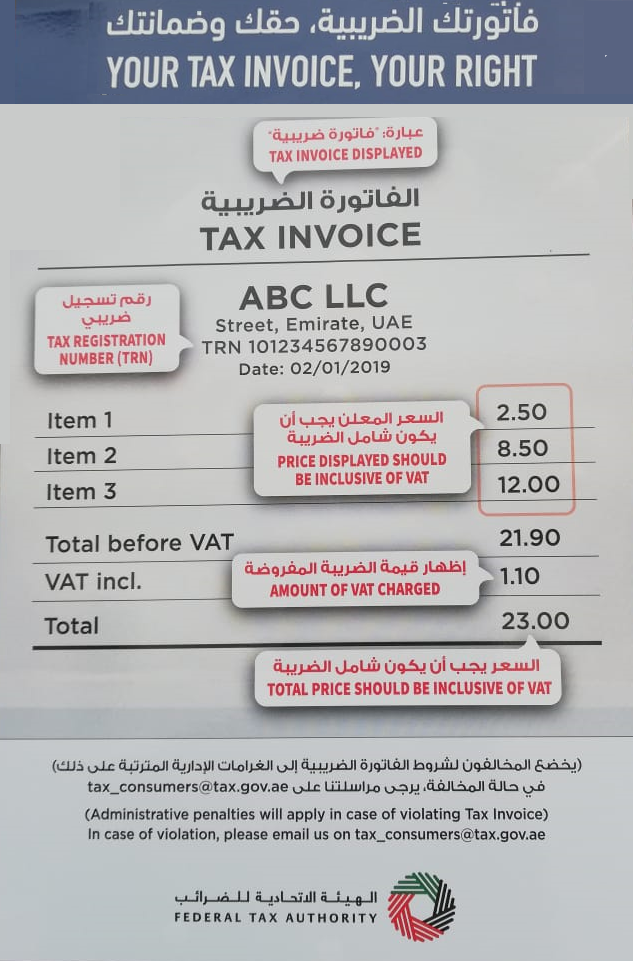

TAX invoice

Tax Invoice

As per Article (59) of Cabinet Decision No. (52) of 2017 on the Executive Regulations of the Federal Decree-Law No (8) of 2017 on Value Added Tax, the tax invoice is a written or electronic document in which the occurrence of a Taxable supply is recorded with the details pertaining to it and this should be issued by the registered supplier on taxable supply of goods and services. The recent public clarification provides the better understanding of the tax invoice format and is given as follows:

- What is the sequential numbering in tax invoices? Is it mandatory?

- When the Invoice raised in any currency other than AED, Is it mandatory to convert the amount to AED? If yes, what amount?

- If the tax invoice is raised in any currency other than AED, then the tax amount payable should be expressed in AED together with the rate of exchange applied.

- The exchange rate should be approved by the central bank as on the date of supply

- What is the date of Issuance of the tax invoice to the recipient of goods or services?

- What is the Penalty for not issuing the tax invoices?

- In case of failure by the taxable person to issue the tax invoice or an alternative document when making any supply, and

- In the case of failure by the Taxable Person to comply with the conditions and procedures regarding the issuance of electronic Tax Invoices and electronic Tax Credit Notes,

- 5000 for each tax invoice or alternative document

- 5000 for each incorrect document.

- What is Simplified Tax Invoice?

The taxable person may issue the simplified tax invoice in either of the following situations:

The taxable person may issue the simplified tax invoice in either of the following situations:

- Where the Recipient of goods or Recipient of services is not a registrant

- Where the Recipient of goods and Recipient of services is a registrant and the consideration for the supply does not exceed AED 10,000.

- What are the documents to be attached with Tax invoice, in case of VAT to be payable by Recipient under RCM?

- A statement that the Recipient is required to account for tax and

- A reference to the relevant provisions under the decree law.

- In which case, there is no requirement for separate tax Invoice?

- When can a taxable person issue an Electronic Tax Invoice

- The Taxable Person must be capable of securely storing a copy of the electronic Tax Invoice in compliance with the record keeping requirements.

- The authenticity of origin and integrity of content of the electronic Tax Invoice should be guaranteed.

- Can a buyer issue the tax invoice for the taxable supply of goods or services?

- The Recipient of the Goods or Services is a Registrant.

- The supplier and the Recipient agree in writing that the supplier shall not issue a Tax Invoice in respect of any supply to which this Clause applies.

- The Tax Invoice shall be in the format as prescribed above.

- The words “Tax Invoice raised by buyer” are clearly displayed on the tax Invoice.

- When can a registered agent issue a tax invoice?

- The agent should be a registrant

- Agent issues the invoice on behalf of the principal, in relation to the supply as if that had been made by the agent

- In this case, the principal shall not issue any tax Invoice

- What are the additional details to be added in tax invoice when supply made to an implementing state?

- The tax registration number (TRN) of the Recipient of Goods or Services issued to him by the competent authority of the Implementing State in which the supply is treated as taking place.

- A statement identifying the supply as between the State and an Implementing State.

- Any other information specified by the Authority.

- What are exceptions to the issue of the tax invoice – (No tax Invoice):

- If there are sufficient records available to establish the particulars of supply and the supply is wholly zero- rated supply.

- When the authority considers and determines that there are sufficient records available to establish that based on the particulars of the supply or class of supplies it is impracticable for the taxable person to issue a tax invoice.

- Where a registrant makes a supply of goods or services through the vending machines, not required to issue a tax Invoice – recent decision.

- A description of the goods or services supplied

- The total consideration and the tax amount charged

- The date of supply of the goods or services

- Highlights of Recent Public Clarification on Tax Invoice: