Jan 24, 2019

Jan 24, 2019  VAT

VAT

TAX invoices

The Tax Invoice is the essential document to be issued in original by a registrant to the recipient when a taxable supply of goods or services is made including a deemed supply (in case, there is no recipient, it must be kept in the taxable person’s records)and in cases where there is either full or partial receipt of consideration prior to the supply.

A valid Tax invoice must contain all of the following details:

-

The words “Tax Invoice” clearly displayed on the invoice.

-

The supplier’s name, address, and Tax Registration Number (TRN) of the Registrant.

-

Where the recipient is VAT registered – name, address, and Tax Registration Number (TRN) of the Recipient.

-

A sequential Tax Invoice number or a unique number which enables identification of the Tax Invoice.

-

The date of issuing the Tax Invoice.

-

The date of supply i.e. tax point if different from the Invoice date.

-

Sufficient description to identify the Goods or Services being supplied and for each description unit price, quantity or volume supplied, rate of tax and the amount payable(expressed in AED) must be shown.

-

The amount of discount offered, if any.

-

The gross amount payable expressed in AED.

-

The Tax amount payable expressed in AED together with the rate of exchange applied where the currency is converted from a currency other than the UAE dirham.Foreign currency exchange rates published by UAE Central bank are available on the following link: https://www.centralbank.ae/en/fx-rates

-

Where the invoice relates to a supply under which the Recipient of Goods or Recipient of Services is required to account for Tax, a statement that the Recipient is required to account for Tax, and a reference to the relevant provision of the Decree-Law

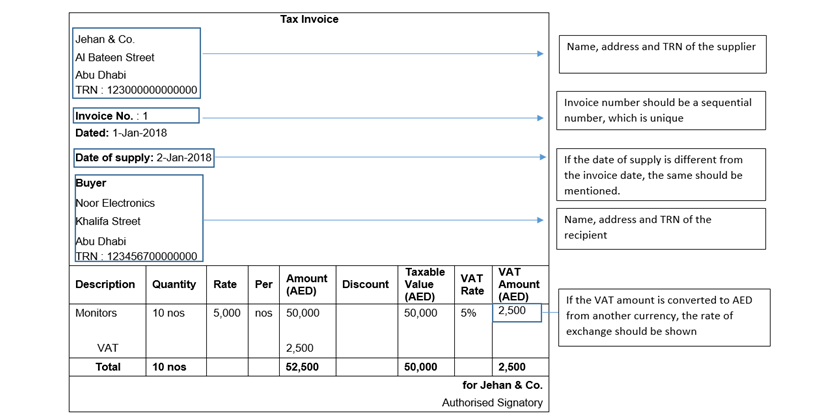

Tax Invoice Format

As per the mandatory details required in a Tax Invoice, a sample format of a Tax Invoice is shown below:

Note: When the Tax Invoice relates to a supply for which the recipient should pay tax, a statement that the recipient is required to account for tax, under Article 48 of the VAT Law should be given in the Tax Invoice.

Simplified Invoices:

The Regulations prescribe that a simplified tax invoice may be issued where the consideration for the supply does not exceed AED 10,000 irrespective of whether the recipient of goods and services is registered or not registered.

Simplified invoice may be issued showing the following details.

-

The words “Tax Invoice” clearly displayed on the invoice.

-

Supplier’s name, address, and Tax Registration Number (TRN)of the Registrant.

-

The date of issuing the Tax Invoice.

-

Sufficient description to identify the Goods or Services being supplied

-

Total amount payable incl. total tax chargeable

Electronic Invoices

The Taxable Person may issue a Tax Invoice by electronic means provided that

-

The Taxable Person must be capable of securely storing a copy of the electronic Tax Invoice in compliance with the record keeping requirements.

-

The authenticity of origin and integrity of content of the electronic Tax Invoice should be guaranteed.

Self Billing

Where a Recipient agrees to raise a Tax Invoice on behalf of a Registrant Supplier in respect of a supply of Goods or Services, that document shall be treated as if it had been issued by the supplier if the following conditions are met:

-

The Recipient of the Goods or Services is a Registrant.

-

The supplier and the Recipient agree in writing that the supplier shall not issue a Tax Invoice in respect of any supply to which this Clause applies.

-

The Tax Invoice shall contain all the particulars of a valid Tax Invoice.

-

The words “Tax Invoice raised by buyer” are clearly displayed on the Tax Invoice.

Where a Tax Invoice is issued by the customer in agreement with the supplier, any invoice issued by the Supplier in respect of that supply shall be deemed not to be a Tax Invoice.

Tax Invoice by Agent

Where an agent who is a Registrant makes a supply of Goods and Services for and on behalf of the principal of that agent, that agent may issue a Tax Invoice in relation to that supply as if that agent had made the supply, provided that the principal shall not issue a Tax Invoice.

Supply of Goods or Services is considered as supplied in an Implementing State

Where the Supply of Goods or Services is considered as supplied in an Implementing State,