Jan 14, 2026

Jan 14, 2026  Corporate Tax

Corporate Tax

UAE Corporate Tax Family Foundation

Need for Family Foundation

- Under the UAE Corporate Tax (CT) Law, natural persons are not subject to Corporate Tax on:

– employment income

– personal investment income and

– real estate investment income (sale, leasing, etc.) - Natural persons often use wealth-holding structures (such as foundations, contractual trusts, trust companies) for asset protection, succession planning, philanthropic and other reasons.

- Such structures may constitute juridical persons for Corporate tax purpose and thereby, become subject to corporate tax.

- To address this, the concept of Family Foundation was provided which grants tax transparency status to such structures, whereby income is considered directly in the hands of beneficiaries rather than at the foundation structure level.

What is Family Foundation?

- Family Foundation is a concept under the UAE CT Law only and is not a legal entity type recognized under UAE’s general legal framework.

- Family Foundation refers to a foundation, trust, or similar arrangement that meets the conditions prescribed under the CT Law to be treated as fiscally transparent.

Conditions under UAE CT Law:

1. Beneficiary Condition:

- Established for the benefit of:

- identified or identifiable natural persons, and/or

- public benefit entity

- No minimum/ maximum number of beneficiaries

- No requirement for beneficiaries to be related or from the same family

2. Principal Activity Condition:

- Principal activity limited to receiving, holding, investing, disbursing or managing the assets or funds associated with savings and investments (e.g., stocks, bonds, real estate)

- Also permitted to disburse funds to beneficiaries, fund charitable activities and make necessary operational expenses.

3. No Business Activity Condition:

- Must not conduct any activity that would be considered as Business or Business Activity if undertaken by a natural person.

- Can only conduct Personal Investment or Real Estate Investment activities – which does not require a license and is not considered as commercial business.

4. No Tax Avoidance Condition:

- Main or principal purpose should not be avoidance of Corporate Tax.

- This Condition may be considered as met where Principal Activity Condition is satisfied.

5. Distribution condition:

- Where beneficiaries include public benefit entities, one of the following conditions must be satisfied:

a) All the income derived by such beneficiary is Exempt Income; or

b) Such beneficiary is Qualifying Public Benefit Entity; or

c) Any Taxable Income derived by Family Foundation is distributed to such beneficiaries within 6 months from the end of relevant Tax Period.

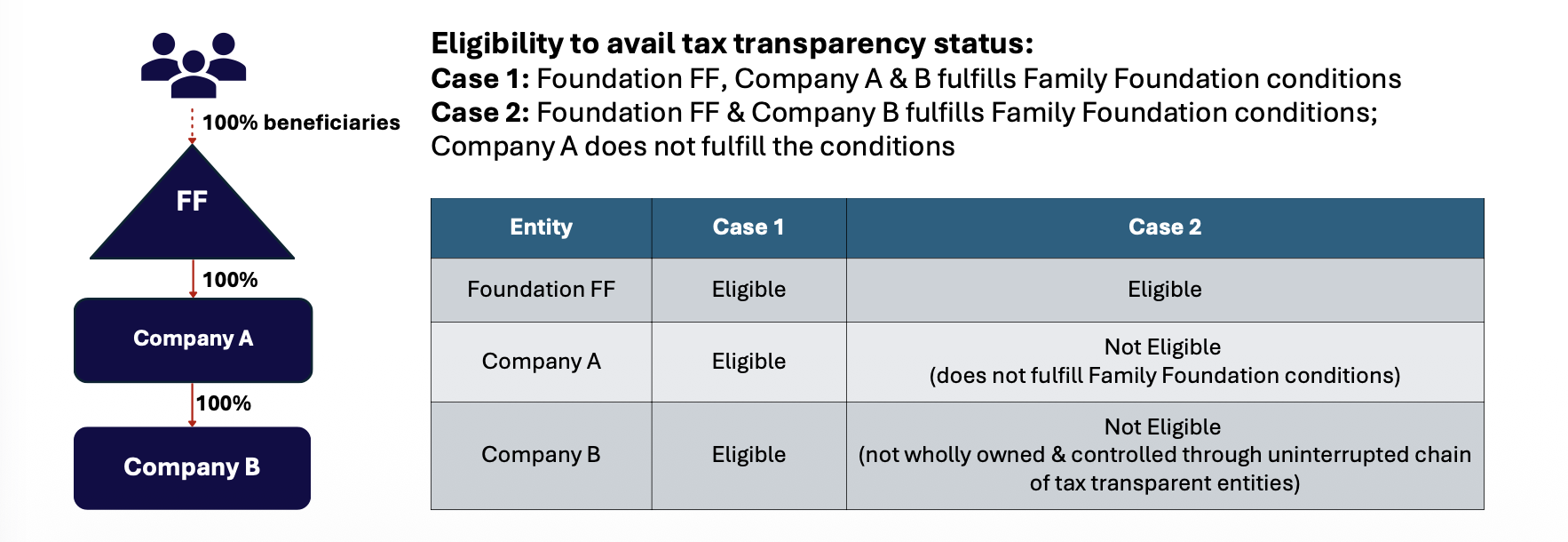

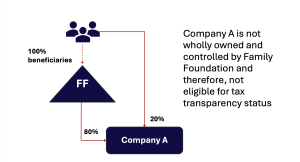

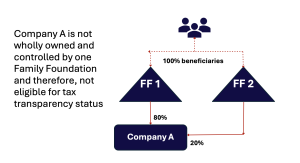

Multi-tier structures:

A juridical person in multi-tier structure may also be considered as fiscally transparent where both the following conditions are continuously met throughout the Tax Period:

– It is wholly owned and controlled by a Family Foundation, either directly or indirectly through an uninterrupted chain of other fiscally transparent entities; and

– It independently meets all Family Foundation conditions under UAE CT Law

Note: No requirement for such juridical persons to have same Financial Year

Tax Effect – Fiscal Transparency:

Once Family Foundation is treated as Unincorporated Partnership

- It is considered fiscally transparent and not subject to Corporate Tax in its own right.

- For Corporate Tax purposes, each beneficiary is deemed to:

– conduct the activities of Family Foundation

– have same status, intention and purpose

– hold assets that Family Foundation holds, and

– be party to any arrangements of Family Foundation - Assets, liabilities, income and expenditure of the Family Foundation are allocated to beneficiaries in proportion to their beneficial interest for each Tax Period

- Tax treatment is assessed at the level of each beneficiary

- Practically, such allocation is required only where any of the beneficiaries is subject to Corporate Tax on such income generated by Family Foundation.

Summary of Compliance Requirements:

| Party | CT Registration | Application for tax transparency | Annual Compliance |

| Foundation | Required | Required before end of relevant Tax Period, unless already treated as Unincorporated Partnership by default (can also be made on behalf of multi-tier juridical persons, to be authorized by respective entities). | Annual Confirmation within 9 months from end of Tax Period (can also be made for multi-tier juridical persons) |

| Multi-tier Entities | Required | Application to be made before end of relevant Tax Period | Annual Confirmation within 9 months from end of Tax Period |

| Natural Person Beneficiary | Required only if conducting separate Business Activities in UAE exceeding AED 1 million total Turnover in Calendar year | Not Applicable | As per respective individual obligations |

| Public Benefit Entity Beneficiary | Required | Not Applicable | As per respective entity obligations |

Key Takeaways:

The UAE Family Foundation regime provides a robust and progressive framework for private wealth structuring under the Corporate Tax Law, enabling tax efficiency while preserving asset protection and succession benefits. When structured and operated in strict compliance with the prescribed conditions, Family Foundation structure allows investment and real estate income to remain tax-neutral at the structure level, with tax treatment consistent with the treatment applicable to ultimate beneficiaries.

However, as a new and evolving regime, the Family Foundation framework is expected to be an area of heightened regulatory focus and interpretational development by the FTA. Some key risk areas could be:

- Broad provisions of General Anti-Avoidance Rules (GAAR) attracting scrutiny where structures appear tax-driven

- Close examination of Principal activity and No business activity test

- Cross-border residency and transparency challenges with foreign authorities

- Failure to meet conditions in any year may trigger audits for earlier periods and result in retrospective tax adjustments denying the benefit

- Multi-tier structures involve greater tax uncertainty as multiple entities are required to fulfill all the conditions and non-compliance at any level may expose the entire structure to FTA scrutiny

Accordingly, it is recommended that taxpayers should approach Family Foundation structures with a substance-driven and compliance-first mindset. This includes maintaining comprehensive documentation evidencing satisfaction of all conditions, ensuring consistency in activities across years, conducting periodic health checks, and closely monitoring evolving FTA guidance and Ministerial Decisions.

With careful planning and proactive compliance management, the Family Foundation regime can serve as a sustainable wealth structuring solution under the UAE Corporate Tax framework.

Download the UAE Corporate Tax Family Foundation pdf by clicking on this link.