Apr 11, 2023

Apr 11, 2023  Corporate Tax

Corporate Tax

UAE Ministerial Circular on Corporate Tax Registration – Exemption

The UAE Ministry of Finance has issued a Ministerial decision No. 43 of 2023 Concerning Exception from Tax Registration for the Purpose of Federal Decree–Law No. 47 of 2022 on the Taxation of Corporations and Businesses.

- Having reviewed the Constitution,

- Federal Law No. 1 of 1972 on the Competencies of Ministries and Powers of the Ministers, and its amendments,

- Federal Decree-Law No. 13 of 2016 on the Establishment of the Federal Tax Authority, and its amendments,

- Federal Decree-Law No. 28 of 2022 on Tax Procedures,

- Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses,

Article (1): Definitions: Words and expressions in this Decision shall have the same meanings specified in the Federal Decree- Law No. 47 of 2022 on the Taxation of Corporations and Businesses (referred to in this Decision as “Corporate Tax Law”) unless the context requires otherwise.

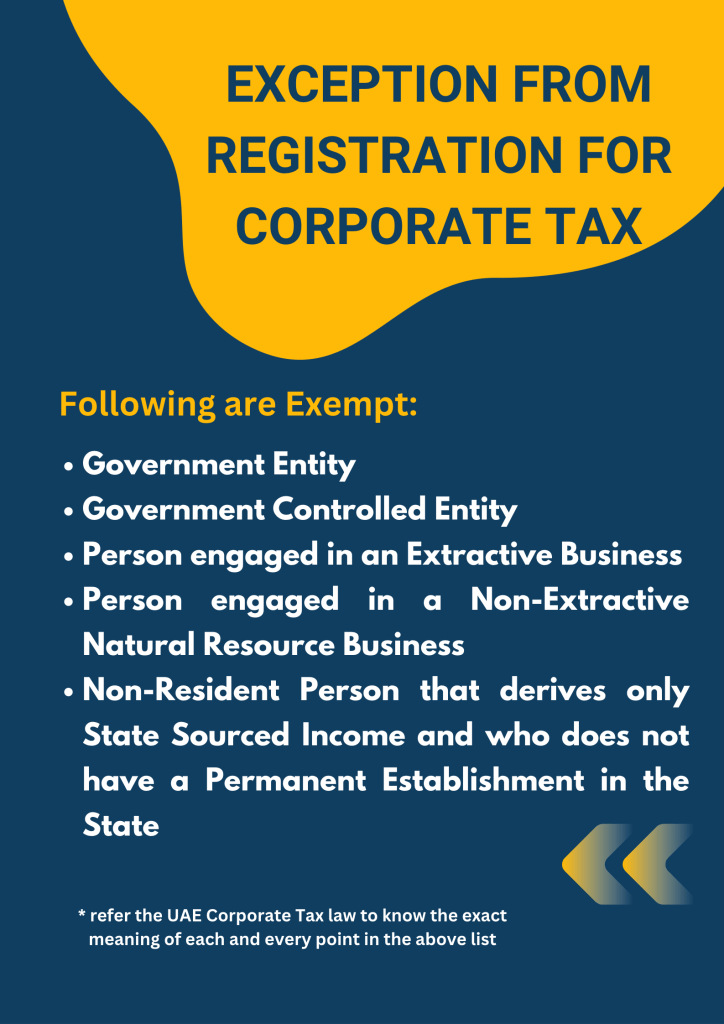

Article (2): Exception from Registration for Corporate Tax:

1. The following Persons shall not register for Corporate Tax with the Authority:

(a) A Government Entity.

(b) A Government Controlled Entity.

(c) A Person engaged in an Extractive Business that meets the conditions of Article 7 of the Corporate Tax Law.

(d) A Person engaged in a Non-Extractive Natural Resource Business, that meets the conditions of Article 8 of the Corporate Tax Law.

(e) A Non-Resident Person that derives only State Sourced Income under Article 13 of Corporate tax Law and that does not have a Permanent Establishment in the State according to the provisions of the Corporate Tax Law.

2. Paragraphs (a) to (d) of Clause (1) of this Article shall be without prejudice to the obligation of the Person to register for Corporate Tax in cases where the Person becomes a Taxable Person under the provisions of the Corporate Tax Law.

All Cabinet Decisions