Apr 08, 2021

Apr 08, 2021  Accounting

Accounting

Profit Margin Scheme v2

{This blog is an updated version of our old blog on ‘Profit Margin Scheme’ present here at: https://www.spectrumaccounts.com/profit-margin-scheme/ and currently the blog is shared in a more useful question & answer format.}

If Profit margin is zero or if a loss is made, the value of the supply is zero for VAT purposes.In other words, there will not be any VAT liability on the Supplier if the profit margin is zero or if it is loss

If Profit margin is zero or if a loss is made, the value of the supply is zero for VAT purposes.In other words, there will not be any VAT liability on the Supplier if the profit margin is zero or if it is loss

In this case, the Input tax will be “Zero”.

In this case, the Input tax will be “Zero”.

- What is a Profit margin Scheme?

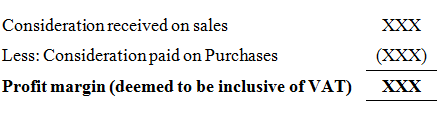

- What would be the Profit margin for Supplier?

If Profit margin is zero or if a loss is made, the value of the supply is zero for VAT purposes.In other words, there will not be any VAT liability on the Supplier if the profit margin is zero or if it is loss

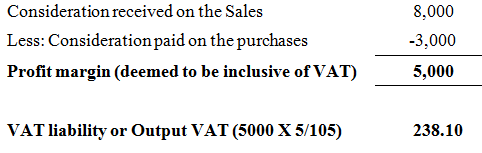

- Give an example for computing the Profit margin and the VAT liability on the same.

In this case, the Input tax will be “Zero”.

- What are the Goods eligible and conditions for applying the Profit Margin Scheme? Only certain goods are eligible to be supplied under the profit margin scheme. Those goods are listed below, but may only be supplied under the scheme where they were subject to VAT before the supply which shall be subject to the profit margin scheme

- Second-hand Goods, meaning tangible moveable property that is suitable for further use as it is or after repair.

- Antiques, meaning goods that are over 50 years old.

- Collectors’ items, meaning stamps, coins and currency and other pieces of scientific, historical or archaeological interest

- only when the above-mentioned eligible goods were purchased from either:

- A Person who is not a Registrant of VAT.

- A Taxable Person who calculated the VAT on the supply by reference to the profit margin i.e., a VAT registered business which already applied the profit margin scheme on the same goods

- When a taxable person made a supply of goods where the input tax was not recovered.

- stock on hand of used goods which were acquired prior to the effective date of VAT applicability in UAE i.e., 1st January 2018(or)

- which have not previously been subject to VAT for other reasons,