Oct 10, 2023

Oct 10, 2023  Corporate Tax

Corporate Tax

Your Guide On Non-Resident Person’s who are Subject to Corporate Tax

The UAE Ministry of Finance has released a guidance on the corporate tax law and implementing decisions on Non-Resident individuals or entities but have a source of income in UAE.

Residency Criteria

A person is a resident person if they conduct business in UAE or is incorporated or otherwise established or recognized in the UAE or is effectively managed in the UAE.

As per the Cabinet Decision No. 85 of 2022 an individual is considered a resident person if –

- If he has been physically present in UAE for a period of 183 days within 12 consecutive months.

- If he is UAE national and holds valid Residence Permit in UAE and meets the followings conditions –

- Permanent Place of Residence in the UAE.

- An employment or Business in the UAE

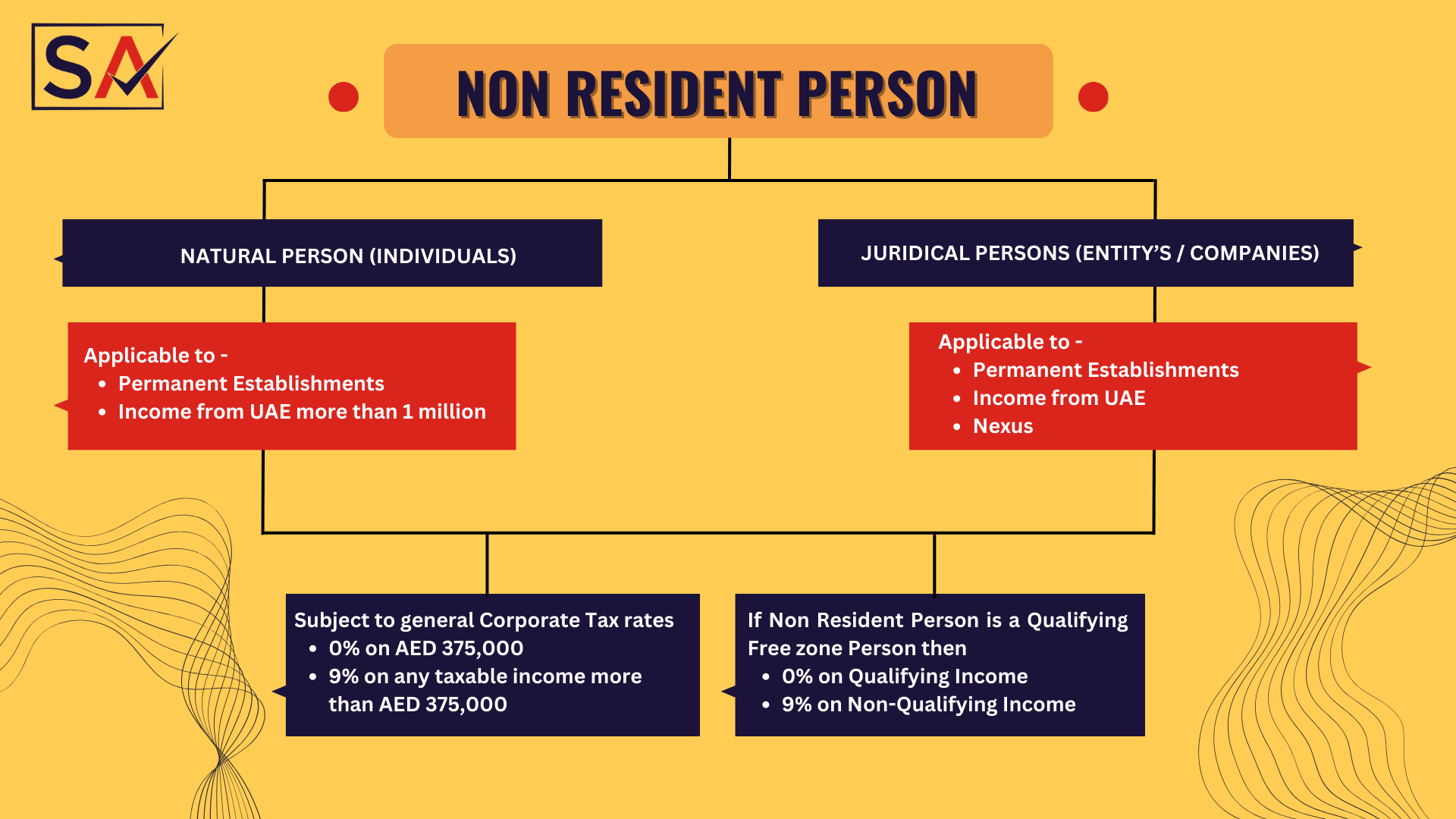

A non-resident person is –

- An individual who is not a resident person but has a Permanent Establishment (PE) from UAE and has a turnover of AED 1 million or more and gets income from UAE.

- An entity who is incorporated outside of UAE has a Permanent establishment in UAE, gets income from UAE or has a nexus.

Individuals who are Non-resident that are subject to Corporate tax

For a non-resident individual who has more than AED 1 million income obtained through Business activities would be subject to corporate tax.

However, the following is not taken into consideration when determining gross taxable income –

- Wages, salary, or any amount received through an employment contract.

- Any return on personal investments

- Income from real estate investments not conducted through a business.

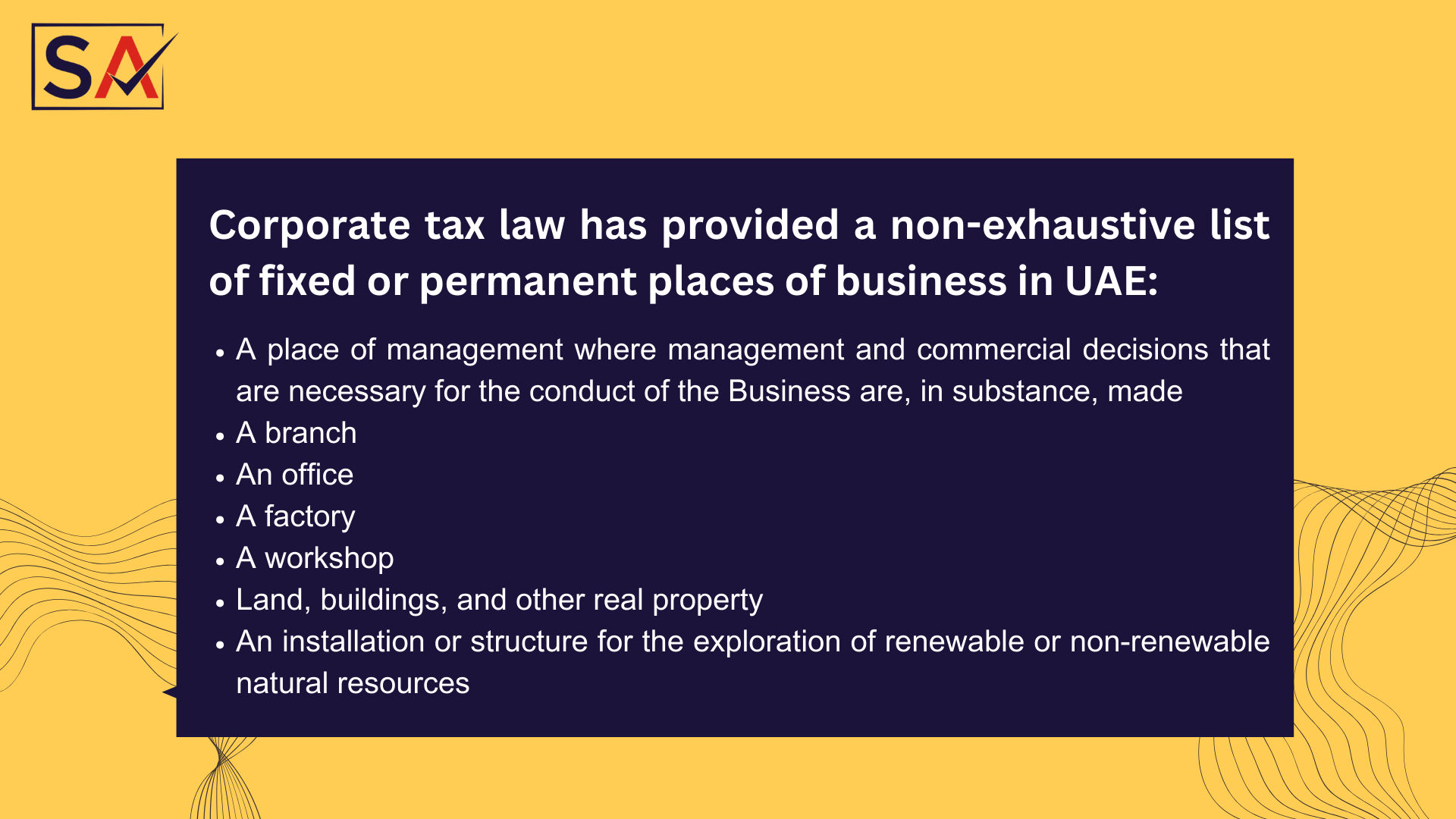

Permanent Establishment

By definition means a fixed or permanent place in UAE through which business is conducted.

There should be a fixed “place of business” in UAE which can be an office, branch or premises which is used to carry out the business activities.

Nexus

Corporate tax is imposed on entities who are non-residents and who have a nexus. The nexus concept does not apply to individuals.

If an entity acquires income through any immovable property in UAE, then it is considered as to have a nexus which means –

- Any area or land over which rights or interest or services can be created.

- Any building, structure or engineering work attached to the land permanently or attached to the seabed.

- Any fixture or equipment which