Sep 05, 2023

Sep 05, 2023  Corporate Tax

Corporate Tax

UAE Corporate Tax – Qualifying Free Zone

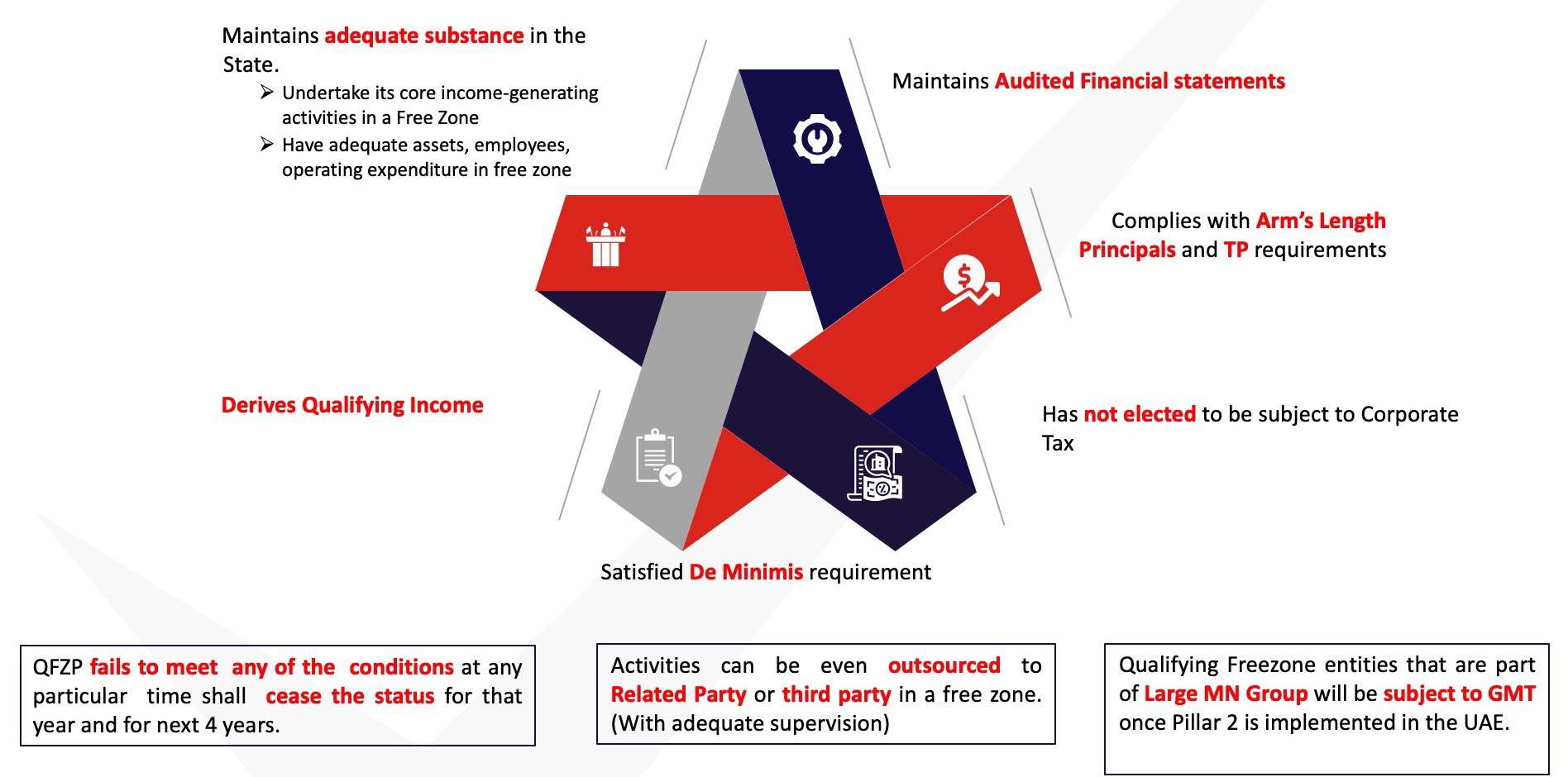

QUALIFYING FREEZONE PERSON – CONDITIONS

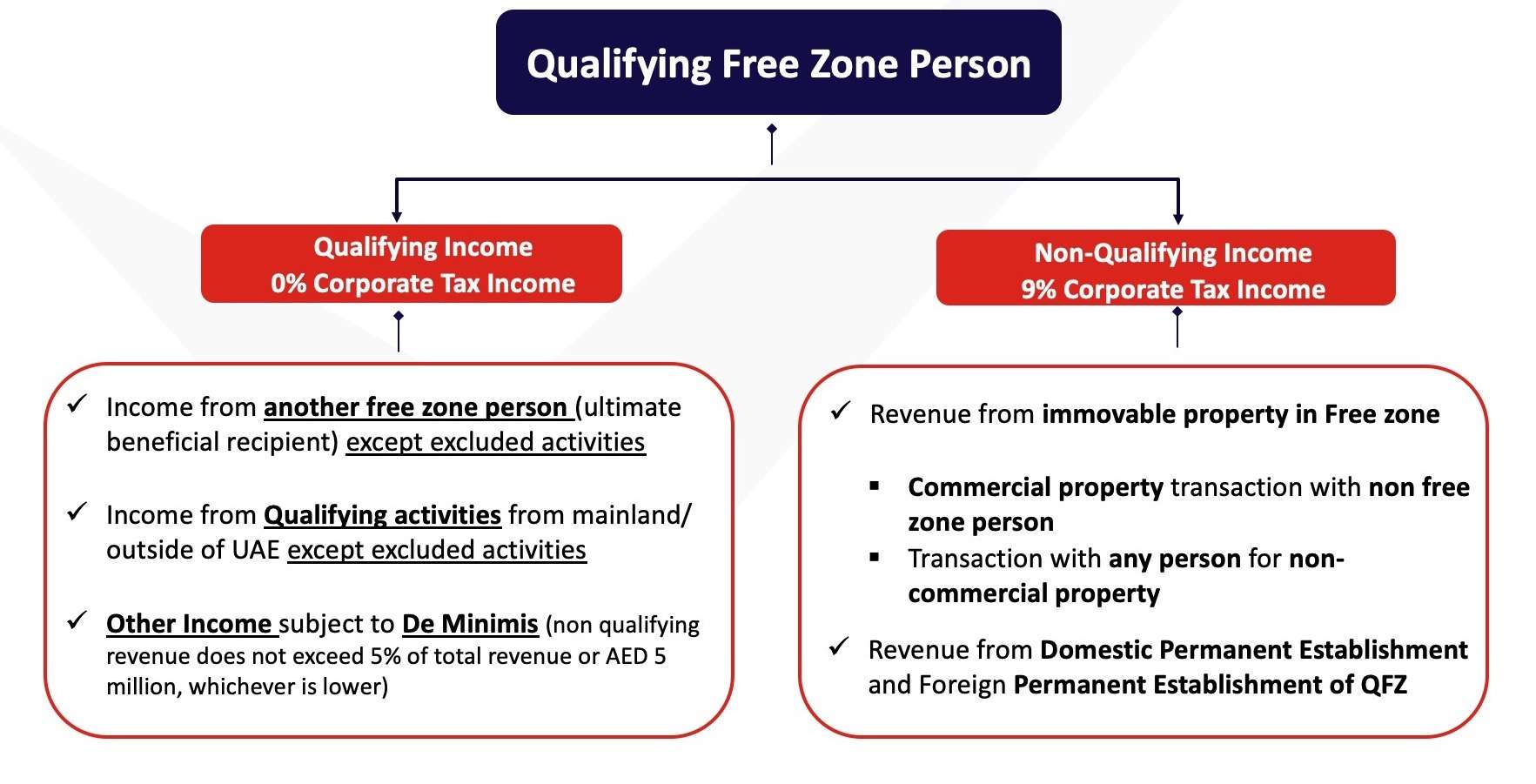

Corporate Tax on Free zone Business- Qualifying & Non qualifying, (Cabinet Decision no. 55 & Ministerial Decision no. 139)

Corporate Tax on Free zone – Qualifying Activities (CD 55 & MD 139)

Qualifying Activities: Goods:- Manufacturing of Goods or materials (PCD: Fully fledged & Contract/ toll manufacturing)

- Processing of Goods or materials

- Distribution of imported goods or materials in or from a Designated Zone to reseller

- Holding of shares and other securities

- Ownership, management and operation of Ships

- Reinsurance services

- Fund management services

- Wealth and investment management services

- Headquarter services to Related Parties

- Treasury and financing services to Related Parties

- Financing and leasing of Aircraft, including engines and rotable components

- Logistics services

- Ancillary activities to above

Corporate Tax on Free zone – Excluded Activities (CD 55 & MD 139)

Excluded Activities (Non-qualifying revenue)- Transaction with Natural Person (except to Ownership or management of ship/ Fund management services/ Wealth & investment management/ Financing & leasing of aircraft)

- Banking activities

- Insurance activities (other than reinsurance)

- Financing and leasing activities, except 1) Financing to related parties & 2) Related to aircraft

- Ownership or exploitation of immovable property, except the transaction with another free zone person related to immovable commercial property in free zone

- Intellectual property assets income

- Ancillary activities to above

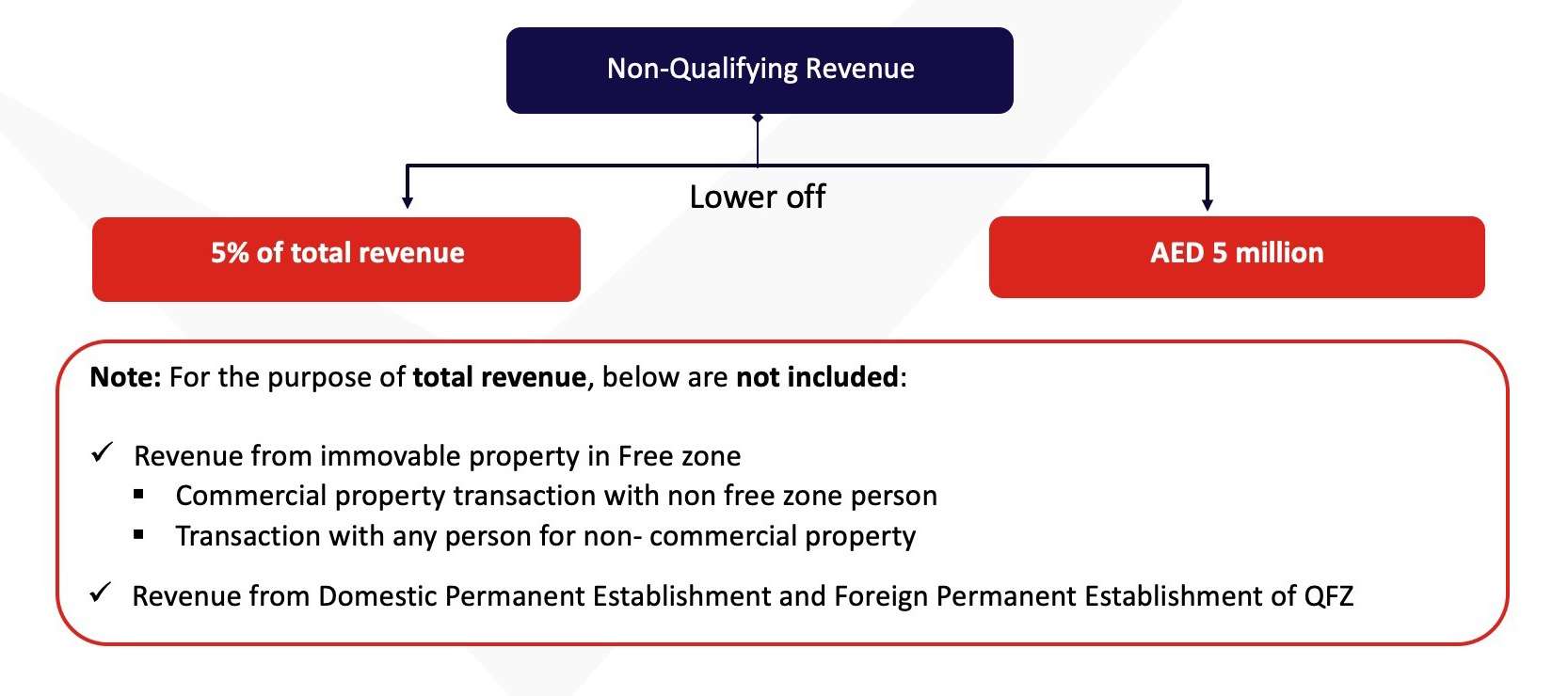

Corporate Tax on Free Zone Business – Qualifying & Non Qualifying – De Minimis Requirement

One of the condition for Qualifying Free Zone Persons (QFZP) is to satisfy De MinimisRequirement, for which Non-Qualifying Revenue should not exceed below limits.

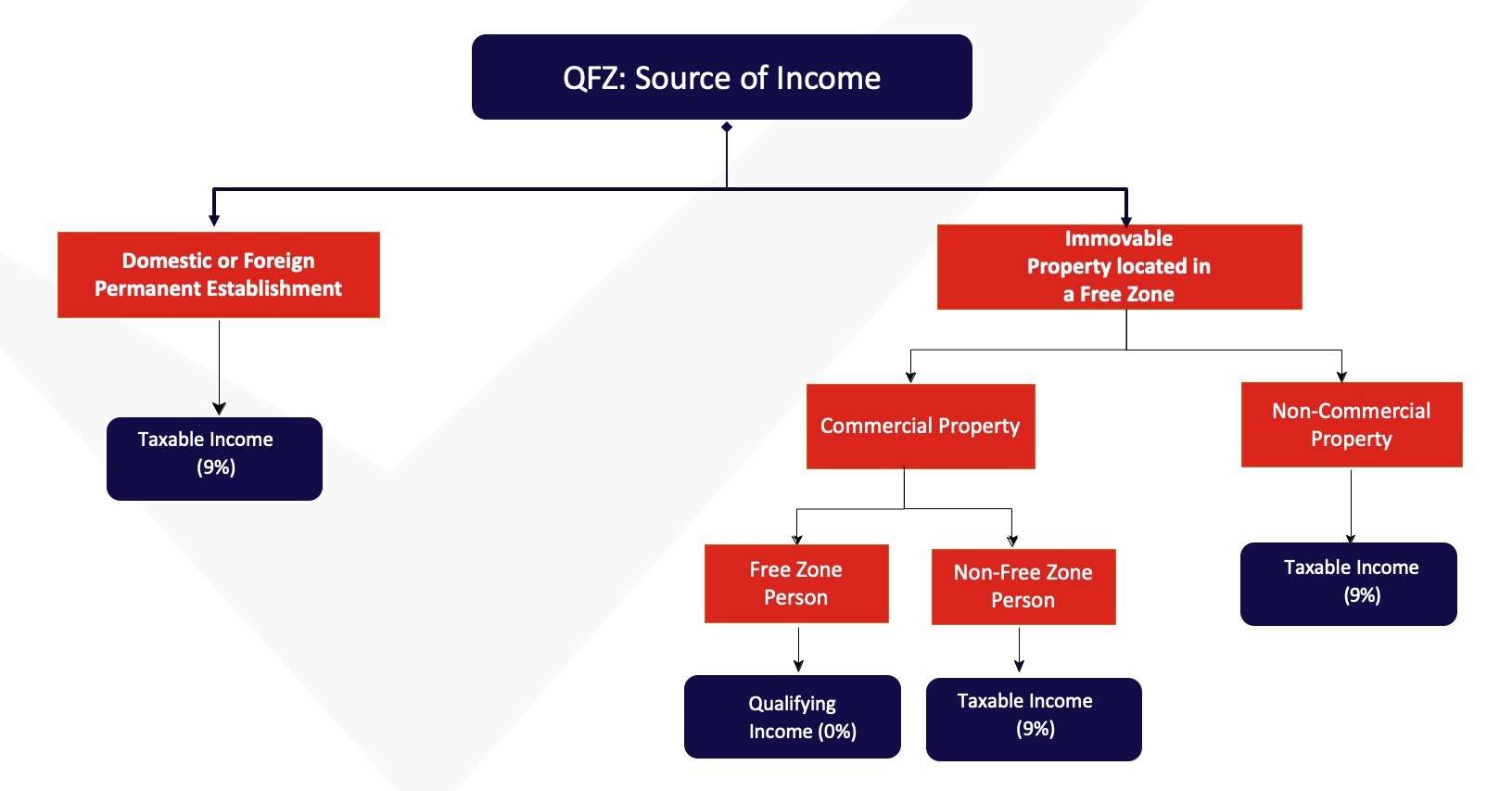

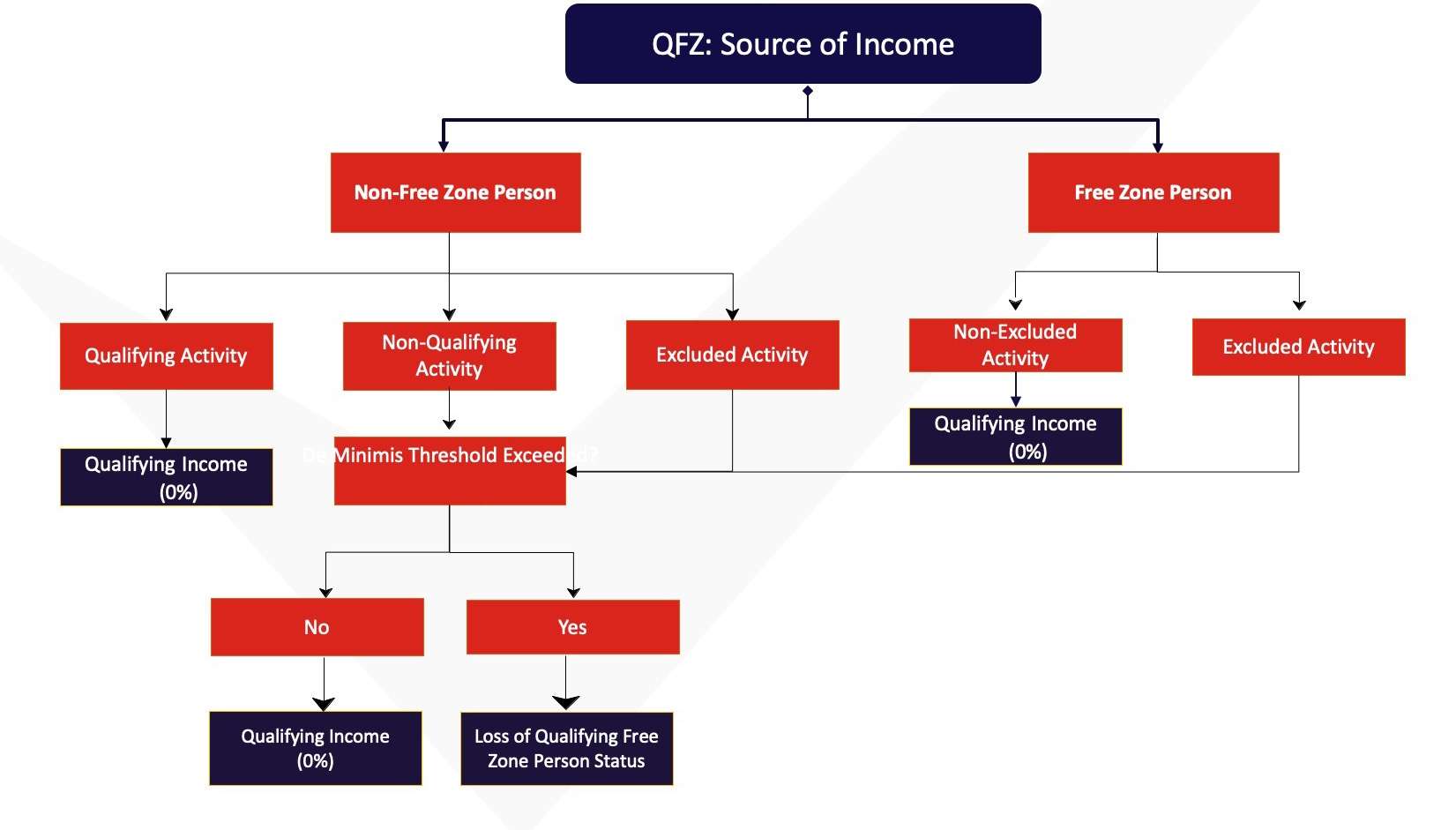

Qualifying Free Zone (QFZ) Taxability

Qualifying Free Zone (QFZ) Taxability