Nov 08, 2023

Nov 08, 2023  VAT

VAT

Cabinet Decision No. 100 of 2023 on Determining Qualifying Income for the Qualifying Free Zone & Ministerial Decision No. 265 of 2023

-

The Ministry of Finance has issued a new Cabinet Decision no. 100 of 2023 which replaces Cabinet Decision no. 55 of 2023.

-

The Ministry of Finance has issued a new ministerial decision no. 265 of 2023 which replaces ministerial Decision no. 139 of 2023.

The important things to note in the new cabinet decision no. 100 of 2023

The definition for Designated Zone has been slightly amended: A designated zone according to what is stated in Federal Decree-Law No. (8) of 2017 on Value Added Tax, and which has been included as a Free Zone in accordance with the Corporate Tax Law.

Qualifying Income

Qualifying income of a Qualifying Free Zone person shall include the following under Article 7 (2) –

- Income generated from doing transactions with a Free Zone person, except for income derived from excluded activities.

- Income generated from transactions with Non-free zone person but only if they are qualifying activities.

- Any other income of the Qualifying Free Zone Person that satisfies the de minimis requirements.

- Income derived from the ownership or exploitation of Qualifying Intellectual Property. (New amendment)

Now the income derived from Qualifying Intellectual Property is a new clause added to the Qualifying Income of a Qualifying Free Zone Person.

What is Qualifying Intellectual Property?

Qualifying Intellectual Property is defined as any Patent, Copyrighted Software, and any right functionally equivalent to a Patent that is legally protected and subject to a similar approval and registration process to a Patent.

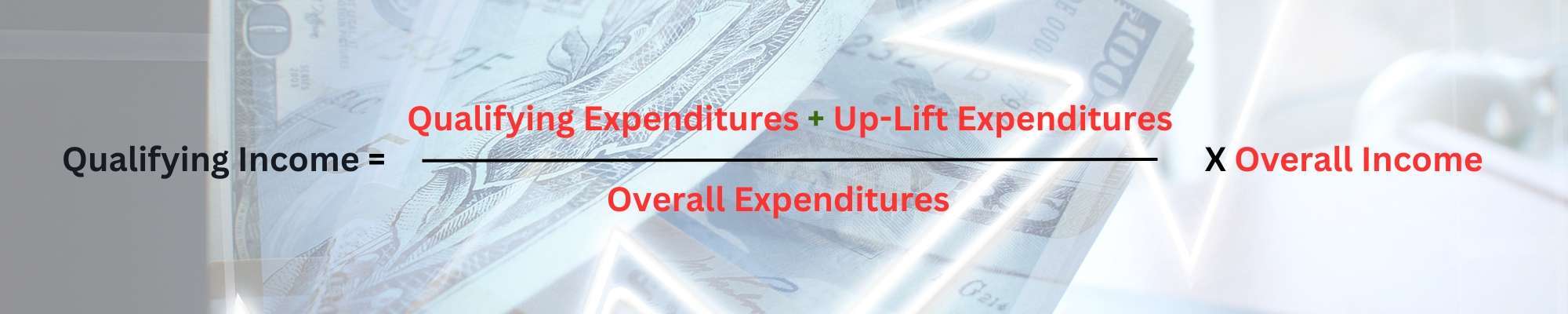

A formula is provided to calculate the amount of Qualifying income derived from Intellectual Property which aims to calculate the portion of income that qualifies for a 0% tax rate.

The formula provided is –

Where –

Qualifying expenditure – Expenditures incurred to fund Research & Development activities conducted by QFZP person or outsourced to person outside state that is not Related Party where the activities are directly connected with the creation, invention, or significant development of Qualifying Intellectual Property.

Overall Expenditures – Total expenditures incurred to fund Research & Development activities which include acquisition costs and qualifying expenditures.

Overall income – means royalties or any other income derived from QIP as determined according to the provisions of the CT Law, including embedded IP income derived from the sale of products and the use of processes directly related to the QIP as determined in accordance with the arm’s length principle.

Uplift Expenditure – means the qualifying expenditure increased by 30%. It should be ensured that the amount of qualifying expenditure after up-lift does not exceed the amount of overall expenditure.

De Minimis requirement

De minimis requirements shall be considered satisfied where income derived from non-qualifying activities is less than 5% of total revenue or AED 5 million whichever is lower.

Non-Qualifying revenue is Revenue derived from –

- Exclude activities.

- Activities that are not Qualifying activities where the other party of the transaction is non-free zone person.

- Transactions with Free Zone person where the person isn’t the beneficial recipient which means that doesn’t consume or enjoy the goods or service provide (New amendment).

Also, the following revenue will not be included in the calculation of non-qualifying revenue and total revenue –

- Revenue derived from immovable property.

- Revenue attributable to domestic Permanent Establishment or foreign Permanent Establishment. These permanent establishments will be treated as if it is a separate independent Person.

- Revenue derived from ownership or exploitation of Intellectual Property (New amendment)

Income derived from permanent establishment of a Qualifying Free Zone Person, or an immovable property located in a Free Zone will be taxed at 9% straight (without any minimum 0% threshold).

As income from Qualifying Intellectual Property is a new amendment in Cabinet decision no. 100 of 2023. So, there are additional clauses for Income derived from Qualifying Intellectual Property which are –

- Qualifying income derived from ownership or exploitation of Qualifying Intellectual Property shall be calculated in accordance with a decision issued in the future by the Ministry of Finance.

- Income derived from the ownership or exploitation of intellectual property that is not Qualifying Intellectual Property and income in excess of Qualifying Income calculated shall be taxed at 9% straight (without any minimum 0% threshold).

Adequate Substance

- A Qualifying Free Zone Person shall undertake its core income generating activities in a Free Zone or Designated Free Zone depending on where such activities are required to be conducted.

They should also have adequate number of assets, qualified full-time employees and also incur adequate number of operating expenditures.

- This core income generating activities can be outsourced to another Person in a Free Zone or Designated Free Zone depending on where such activities are required to be conducted.

- For Qualifying Intellectual Property, it can be outsourced to another Person in UAE or another Person who is not a Related Party outside UAE.

The important things to note in the new ministerial decision no. 265 of 2023

As mentioned in cabinet decision no. 100, Article 3, there