Apr 16, 2020

Apr 16, 2020  ESR and CbCR

ESR and CbCR

The UAE Economic Substance Regulations

The UAE introduced Economic Substance Regulations pursuant to Cabinet of Ministers Resolution No.31 of 2019(“Regulations”) on 30 April 2019. Guidance on the application of the Regulations was issued on 11 September 2019 pursuant to Ministerial Decision No. 215 of 2019 (“Guidance”).

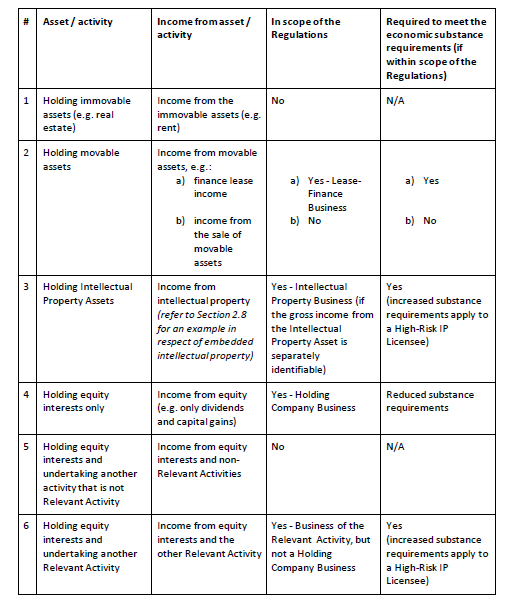

The Regulations require companies and other business forms registered in the UAE that carry on one or more “Relevant Activities” (together, “Relevant Activities”), to have economic substance in the UAE in relation to these activities, and to comply with notification and return filing obligations. Such businesses are referred to in the Regulations and this document as “Licensees”.

To support UAE businesses in understanding the scope and application of the Regulations, this article provides additional guidance on the “Relevant Activities” and their associated “Core Income-Generating Activities” (“CIGAs”).

Core Income-Generating Activities of a Holding Company Business

The CIGAs of a Holding Company Business are all activities related to acquiring and holding shares or equitable interests in other companies, provided that

Core Income-Generating Activities of a Holding Company Business

The CIGAs of a Holding Company Business are all activities related to acquiring and holding shares or equitable interests in other companies, provided that

- Assessment of whether an entity is undertaking a Relevant Activity

- Banking Businesses

- Insurance Businesses

- Investment Fund Management Businesses

- Lease-Finance Businesses

- Headquarters Businesses

- Shipping Businesses

- Holding Company Businesses

- Intellectual Property Businesses

- Distribution and Service Centre Businesses

- Section 3.1: Banking Business;

- Section 3.4: Lease-Financing Business;

- Section 3.5: Headquarters Business; and

- Section 3.9: Distribution and Service Centre Business.

- Relevant Activities and Core Income-Generating Activities

- the making or giving of loans, advances, overdrafts, guarantees or similar facilities; or

- the making of investments,

- ‘Raising funds, managing risk including credit, currency and interest risk’ – In addition to accepting deposits from the public, raising funds also includes raising capital, issuing bonds or going to the money markets. A Banking Business’ risk management activities would be aimed at ensuring the capital base of the Licensee is not eroded and to control the cost of funds. The key functions and related decision-making in respect of these activities are expected to be performed in the UAE.

- ‘Taking hedging positions’ – Where the Licensee mitigates risks by taking opposing or offsetting positions, the Licensee must be able to demonstrate that the related activities and decisions making take place in the UAE.

- ‘Providing loans, credit or other financial services to customers’ – A Banking Business would be expected to lend or otherwise invest its customer deposits and other available funds. The term “customer” is not limited to individuals, but also includes corporations and other financial institutions.

- ‘Managing capital and preparing reports to investors or any government authority with functions relating to the supervision or regulation of such business’ – The banking sector is highly regulated, and involves various reporting to regulators and investors. The Licensee is expected to perform and oversee its reporting related functions and activities in the UAE.

- ABC Bank (UK) offers current accounts, savings accounts, loans, credit cards, and other products and services to individual and corporate customers through a number of branches in the UAE. ABC Bank clearly undertakes a Banking Business in the UAE and is subject to the Regulations.

- PQR is a UAE branch of the Investment Banking division of the STV Banking Group. The activities of PQR include underwriting new debt and equity securities, facilitating and advising buyers and sellers on mergers and acquisitions, and marketing financial products. Whilst permitted under its UAE investment banking license to accept deposits whose maturities are at least two years, PQR’s funding is limited to borrowings from its head office and from other banks. PQR would not be considered as carrying on a Banking Business and be subject to the Regulations on this basis.

- MNO is the UAE branch of the JKL Banking Group that provides retail and corporate banking services globally. The activities of MNO are limited to providing UAE and regional clients with assistance and advice regarding the JKL Banking Group’s products and services, including assistance in the process of opening accounts with JKL Banking Group entities that are based outside of the UAE. MNO LLC is not considered to undertake a Banking Business by virtue of being in the same corporate group, and assistance in the opening of bank accounts would not be considered as conducting deposit taking activities. MNO may, however, be considered as undertaking a “Distribution and Service Centre Business” and be within the scope of the Regulations on this basis.

- ‘Predicting and calculating risk’ – This CIGA involves the determination of the quantification and likelihood of the insured event occurring and the likely costs, and ensuring that the premiums charged are commensurate with the risks accepted.

- ‘Insuring or re-insuring against risk and providing Insurance Business services to clients’ – This CIGA includes insuring policyholders against specific risks and providing reinsurance to primary insurers.

- ‘Underwriting insurance and reinsurance’ – This CIGA refers to the evaluation and analysis of the risks of an insurance policy, and establishing the pricing for accepted insurable risks.

- First Life LLC (UAE) provides life, health and car insurance in and from the UAE, and is regulated as an Insurer by the UAE Insurance Authority. First Life LLC clearly undertakes an Insurance Business and is subject to the substance requirements.

- IntermediaryCo LLC (UAE) is an insurance intermediary that assists and represents consumers in the placement and purchase of insurance, and provides services to insurance companies to facilitate and complement the insurance placement process. IntermediaryCo is regulated as an

- ‘Taking decisions on the holding and selling of investments‘ – This CIGA involves the independent consideration, deliberation and making of investment and divestment decisions. A licensee that is merely implementing decisions of another entity with respect to the holding and selling of investments without independent evaluation before taking steps or decisions to effect the investment or divestment decisions taken, does not perform the CIGA. It is a commercial reality that the directors or members of an investment committee may not all be based in the UAE or be physically present in the UAE when investment and divestment decisions are taken. However, for this CIGA to be seen as taking place in the UAE, the majority of those making the decisions should be physically present in the UAE when the decisions are made.

- ‘Calculating risk and reserves’ – Managing an Investment Fund involves identifying, measuring, monitoring and controlling risks attributable to the Investment Fund’s operations and investments. This CIGA refers to activities in respect of risks for the Investment Fund as a whole, as opposed to isolated risk calculations for one area of applicable risk that does not take into

- ‘Taking decisions on currency or interest fluctuations and hedging positions’ – This CIGA refers to the activities required to determine if the Investment Fund is exposed to, or if it is in the best interests of the Investment Fund to enter into, hedging arrangements against currency or interest fluctuations, and taking relevant decisions regarding those determinations. As with the other CIGAs, the Investment Fund Manager is expected to perform this activity on a holistic basis, taking into account the Investment Fund’s overall position. Isolated decisions involving specific investments are not sufficient to meet the CIGA requirement.

- ‘Preparing reports to investors or any government authority with functions relating to the supervision or regulation of such business’ – This CIGA does not require the Licensee to perform the administrative task of compiling the various routine annual or quarterly reports. However, the Licensee is expected to oversee this work from the UAE and to ensure the necessary systems and processes are in place, including the contractual arrangement with any third party administrator. The Licensee is also expected to have the ultimate responsibility for the reporting, and to have the necessary understanding and knowledge to accurately convey the position of the Investment Fund(s) at any time.

- ‘Agreeing funding terms’ – This CIGA relates to the funding of the Licensee itself, and includes agreeing the type of funding (e.g. equity, preference shares, debt, etc.), the quantum of funding, the currency, the rates of interest payable, the security given (if any), and any covenants.

- ‘Identifying and acquiring assets to be leased (in the case of leasing)’ – This CIGA refers to the activity of identifying and verifying suitable assets to purchase and then rent to a hirer or lessee for an agreed period, including negotiating the acquisition and the terms of the supply of the assets to be leased or hired.

- ‘Setting the terms and duration of any financing or leasing’ – The Licensee is expected to have the authority (within certain parameters, where applicable) and undertake the negotiation of

- ‘Monitoring and revising any agreements’ – This CIGA could include obtaining data about a borrower or lessee (or the group to which they belong), testing compliance against covenants, extending the duration or the changing of other terms of the financing provided, and ensuring all relevant information is fed into the decision making process and any amended financing terms.

- ‘Managing any risks’ – This CIGA refers to activities in relation to debt collection, monitoring and maintaining the conditions of the underlying leased assets (in the case of leasing), entering into swap and hedging arrangements, and developing and implementing strategies to reduce or spread risks.

- STU LLC (UAE) lends AED 1,000,000 to its subsidiary, VWX LLC, at a 10% interest rate per annum. In respect of the interest bearing shareholder loan made by STU LLC, it is considered engaged in a Lease-Finance Business (specifically, financing).

- STU LLC subsequently assigns the AED 1,000,000 loan to YZ LLC (UAE), another group company.

- TradeCo LLC (UAE) sells office supplies and allows its customers a 45-day payment term on invoices. If customers do not pay within 45 days, TradeCo charges late payment interest.

- TreasuryCo LLC (UAE) is part of the JMR group and acts as the central treasury center for the group. TreasuryCo enters into external borrowing arrangements and on lends the borrowed funds to group companies at the same interest rate it is being charged by the external funders.

- The Licensee takes on the responsibility for the overall success of the group; or

- The Licensee is responsible for an important aspect of the overall group’s performance.

- ‘Taking relevant management decisions’ – This CIGA refers to making decisions on the substantive functions and significant risks for group companies, such as decisions on material acquisitions and purchases, the group companies’ sales and marketing strategy, product development, business process standardization, etc. For a decision to be seen as being made in the UAE, the majority of those making the decision should be physically present in the UAE.

- ‘Incurring operating expenditures on behalf of group entities’ – This CIGA could include engaging specialist advice or procuring technology on behalf of the group as a whole, or purchasing significant assets or specific services for or on behalf of group companies.

- ‘Coordinating group activities’ – This CIGA refers to ensuring that activities such as marketing, HR, IT, finance, tax etc. are coordinated and organised in a way that produces the best outcome for the group as a whole as opposed to individual group companies.

- PLC LLC (UAE) is part of a multinational group with subsidiaries around the world. Each of the senior management team based in the UAE has responsibility for a different region, and regularly spend time at the subsidiaries with the local management teams providing strategic direction and helping manage material risks. In addition, PLC LLC supports the group in managing risk through the procurement of external advice centrally, and the associated costs are shared amongst the group.

- FGH LLC (UAE) is part of a UK headquartered group and has subsidiaries in the Kingdom of Saudi Arabia (“KSA”). Whilst the senior management of FGH LLC have regular contact with the management of the KSA subsidiaries on the performance of their business and to share insights from the group, and FGH LLC (in its capacity as shareholder) has certain rights and influence in respect of the management and operations of the KSA subsidiaries, the KSA subsidiaries follow the strategic direction and manage risks in line with the corporate policy set by the headquarters based in the UK.

- vessels used for fishing;

- vessels that are “small” (i.e. tonnage does not exceed ten tonnes); and

- leisure vessels (e.g. cruise ships and private yachts).

- the rental on a charter basis of ships

- the sale of tickets or similar documents

- the use, maintenance or rental of containers

- the management of the crew of ships.

- ‘Managing crew (including hiring, paying and overseeing crew members)’ – This CIGA could include the sourcing, recruitment, selection, deployment, scheduling, training, and on-going management of the crew deployed on the vessels, including the associated administration (payroll, insurance, tax and social security withholding) and logistics (travel arrangements, temporary accommodation etc.).

- ‘Overhauling and maintaining ships’ – This CIGA involves having responsibility for, and the related decision making in respect of, the lifting of vessels from the water for maintenance and the general maintenance of ships.

- ‘Overseeing and tracking shipping’ – This CIGA refers to the management and oversight of the logistical aspects of the international transportation of cargo and passengers by ship, including overseeing and managing ship movements.

- ‘Determining what goods to order and when to deliver them, organising and overseeing voyages’ – This CIGA involves activities to determine how a ship is to be utilised, the types of cargo acceptable and the scheduling of the delivery of such cargos, managing the logistical aspects of the operation of ships, determining which routes to use, and ensuring necessary contingency arrangements are in place.

- Water LLC owns a passenger ship and its business is to operate that ship in international traffic to carry passengers from the UAE to other Middle East countries. Water LLC is within the scope of a Shipping Business because it operates a ship in international traffic for the transport of passengers.

- Charter LLC owns a ship and charters it on a bareboat basis to Cargo LLC that uses and operates the ship to carry cargo from the UAE to other countries.

Core Income-Generating Activities of a Holding Company Business

The CIGAs of a Holding Company Business are all activities related to acquiring and holding shares or equitable interests in other companies, provided that